|

|

Post by imSINGLEruRICH on Aug 19, 2018 9:56:19 GMT -5

Aug 18, 2018 23:42:39 GMT -4 PRECISION said:

White Hats Report #66 – Benghazi, the REAL story

Often times, intel comes to us in various forms, requiring us to parse it, vet it, sort it, collate it, confirm it and then compose a release/report for public consumption. In this instance, the intel will be released as is for it needs no process as described above. Some of these facts were already known, others not, but now we have the full picture of what happened in Benghazi and why. It can only be described as another example of cabal skullduggery only this time the unauthorized, illegal op went sideways and three patriots in addition to one of the cabal’s own was sacrificed to cover up the criminality.

Incidents like this remind us why we elected Trump.

We ask everyone to link, repost and/or spread this article far and wide, we need to get this to the masses. And now, the REAL story:

Why Benghazi Went Bad

Ambassador Stevens was sent to Benghazi to secretly retrieve US made Stinger Missiles that the State Dept had supplied to Ansar al Sharia in Libya WITHOUT Congressional oversight or permission.

Sec State Hillary Clinton had brokered the Libya deal through Ambassador Stevens and a Private Arms Dealer named Marc Turi, but some of the shoulder fired Stinger Missiles ended up in Afghanistan where they were used against our own military.

On July 25th, 2012, a US Chinook helicopter was downed by one of them. Not destroyed only because the idiot Taliban didn’t arm the missile. The helicopter didn’t explode, but it had to land and an ordnance team recovered the missile’s serial number which led back to a cache of Stinger Missiles kept in Qatar by the CIA.

Obama and Hillary were in full panic mode, so Ambassador Stevens was sent to Benghazi to retrieve the rest of the Stinger Missiles. This was a “do-or-die” mission, which explains the Stand Down Orders given to multiple rescue teams during the siege of the US Embassy.

It was the State Dept, NOT the CIA, that supplied the Stinger Missiles to our sworn enemies because Gen. Petraeus at CIA would not approve supplying the deadly missiles due to their potential use against commercial aircraft. So then, Obama threw Gen. Petraeus under the bus when he refused to testify in support of Obama’s phony claim of a “spontaneous uprising caused by a YouTube video that insulted Muslims.”

Obama and Hillary committed TREASON!

THIS is what the investigation is all about, WHY she had a Private Server, (in order to delete the digital evidence), and WHY Obama, two weeks after the attack, told the UN that the attack was the result of the YouTube video, even though everyone KNEW it was not.

Furthermore, the Taliban knew that the administration had aided and abetted the enemy WITHOUT Congressional oversight or permission, so they began pressuring (blackmailing) the Obama Administration to release five Taliban generals being held at Guantanamo.

Bowe Bergdahl was just a useful pawn used to cover the release of the Taliban generals. Everyone knew Bergdahl was a traitor but Obama used Bergdahl’s exchange for the five Taliban generals to cover that Obama was being coerced by the Taliban about the unauthorized Stinger Missile deal.

So we have a traitor as POTUS that is not only corrupt, but compromised, as well and a Sec of State that is a serial liar, who perjured herself multiple times at the Congressional Hearings on Benghazi. Perhaps this is why no military aircraft were called upon for help in Benghazi: because the administration knew that our enemies had Stinger Missiles that, if used to down those planes, would likely be traced back to the CIA cache in Qatar and then to the State Dept’s illegitimate arms deal in Libya.

References:

Video Placeholder

Video Placeholder

Obama’s DOJ drops charges against Turi

August 17th, 2018 | Category: Uncategorized

|

|

|

|

Post by imSINGLEruRICH on Aug 31, 2018 12:42:13 GMT -5

Posted by nada999999

yesterday at 12:45amGuess Naked Short Selling is not a myth. Finra officially fined some brokers imho Posted by elmarcoYeah the time period they shorted was 2012- 2015. They are just getting fined now. What happened to all the Brokers and market makers that Naked Shorted back in 2004 and 2005 and beyond? Nothing happened to them. They got away with it. We are made to wait 14 fricken years! What a joke of Justice.’On top of it all CMKX shareholders knew tons of Information about NSS and we went silent. Shame on us and Shame on me. woodrot

DIAMOND JEDI

Brokers Fined $5.5 Million for Naked Short Selling yesterday at 10:00am

diamondsandgemms likes this Good post Elmarco …. And to top it off … I can't find facts to back up my thoughts, but I'm willing to bet 100 million plus CMKX shares that the company that was fined $5.5 million likely made $50 or $60 million on their N/S activities …. probably tax free ta'boot …. and whaooooo nelly they were fined !! Probably used the "Madoff Exception" too. Madoff exception link below www.dailykos.com/stories/2009/2/5/693457/- New term... Joketice. As I am ….. bewilderedly wondering ………………………………………………… why I don't puke more often when I hear about this stuff.

sportsman93306

DIAMOND JEDI WARLORD

Post by sportsman93306 on 16 hours agoOne comment and one question. Comment.,,,,. The SEC wanted to remove the terminology ,'naked short' from their vocabulary, and wanted to use ,FTD'. They have to eat their own word. Question.... Does anybody know, how many shares were naked shorted? (fine was $5.5 million). Best wishes |

|

|

|

Post by imSINGLEruRICH on Sept 8, 2018 13:49:14 GMT -5

stump1

King of Diamonds

Post by stump1 on 3 hours ago

▶Anonymous 09/07/18 (Fri) 18:07:05 7c7dfc (1) No.2925851>>2925921 >>2926040 >>2926112 >>2926500 >>2926508 >>2926521

File (hide): bc1640290d70d92⋯.png (6.09 MB, 2000x4386, 1000:2193, McCainsTribunal.png) (h) (u)

Fullsized image

Think Logically.

(((sleeper cells)))

Trump controls IT ALL.

Including sleeper cells.

Including word "lodestar".

Including McCain "funeral".

Including MSM self-destruct.

Including NYT OpEd piece.

Including the entire Congress.

Including Comey, Mueller, RR.

Think Mirror. Mirror your thinking.

They are our hostages.

No deals. Hostages, yes.

They are doing exactly as instructed.

Exactly on the schedule we gave them.

After they were convicted in Tribunals.

After 12/21/17 Executive Order.

Justice will be served at the right time.

But the Republic must be awakened first.

Re-Read this graphic very carefully.

Especially the part about HOSTAGES.

Think Logically.

(((sleeper cells)))

Trump controls IT ALL.

Including sleeper cells.

Including word "lodestar".

Including McCain "funeral".

Including MSM self-destruct.

Including NYT OpEd piece.

Including the entire Congress.

Including Comey, Mueller, RR.

Think Mirror. Mirror your thinking.

They are our hostages.

No deals. Hostages, yes.

They are doing exactly as instructed.

Exactly on the schedule we gave them.

After they were convicted in Tribunals.

After 12/21/17 Executive Order.

Justice will be served at the right time.

But the Republic must be awakened first.

Re-Read this graphic very carefully.

Especially the part about HOSTAGES.

|

|

|

|

Post by imSINGLEruRICH on Sept 8, 2018 13:56:41 GMT -5

[quote timestamp="1536367055" source="/post/901659/thread" [/quote] |

|

|

|

Post by 3bid on Sept 14, 2018 13:26:15 GMT -5

Washington’s Silent Weapon for Not-so-quiet Wars

20.08.2018 Author: F. William Engdahl | NEO

Today by far the deadliest weapon of mass destruction in Washington’s arsenal lies not with the Pentagon or its traditional killing machines. It’s de facto a silent weapon: the ability of Washington to control the global supply of money, of dollars, through actions of the privately-owned Federal Reserve in coordination with the US Treasury and select Wall Street financial groups. Developed over a period of decades since the decoupling of the dollar from gold by Nixon in August, 1971, today control of the dollar is a financial weapon that few if any rival nations are prepared to withstand, at least not yet.

Ten years ago, in September, 2008, US Treasury Secretary, former Wall Street banker Henry Paulson, deliberately pulled the plug on the global dollar system by allowing the mid-sized Wall Street investment bank, Lehman Bros go under. At that point, with aid of the infinite money-creating resources of the Fed known as Quantitative Easing, the half-dozen top banks of Wall Street, including Paulson’s own Goldman Sachs, were rescued from a debacle their exotic securitized finance created. The Fed also acted to give unprecedented hundreds of billions of US dollar credit lines to EU central banks to avert a dollar shortage that would clearly have brought the entire global financial architecture crashing down. At the time six Eurozone banks had dollar liabilities in excess of 100% of their country GDP.

A World Full of Dollars

Since that time a decade ago, the supply of cheap dollars to the global financial system has risen to unprecedented levels. The Institute for International Finance in Washington estimates the debt of households, governments, corporations and the financial sector in the 30 largest emerging markets rose to 211% of gross domestic product at the start of this year. It was 143% at the end of 2008.

Further data from the Washington IIF indicate the scale of a debt trap that is only in early stages of detonating across the less-advanced economies from Latin America to Turkey to Asia. Excluding China, emerging market total debt, in all currencies including domestic, has nearly doubled from 15 trillion dollars in 2007 to 27 trillion dollars at end of 2017. China debt in the same time went from 6 trillion dollars to 36 trillion dollars according to IIF. For the group of Emerging Market countries, their debts denominated in US dollars has grown to some 6.4 trillion dollars from 2.8 trillion dollars in 2007. Turkish companies now owe almost 300 billion dollars in foreign-denominated debt, over half its GDP, most in dollars. Emerging markets preferred the dollar for many reasons.

As long as those emerging economies were growing, earning export dollars at a rising rate, the debt was manageable. Now all that’s beginning to change. The agent of that change is the world’s most political central bank, the US Federal Reserve, whose new chairman, Jerome Powell, is a former partner of the spooky Carlyle Group. Arguing that the domestic US economy is strong enough that they can return US dollar interest rates to “normal,” the Fed has begun a titanic shift in dollar liquidity to the world economy. Powell and the Fed know very well what they are doing. They are ratcheting up the dollar screws to precipitate a major new economic crisis across the emerging world, most especially from key Eurasian economies such as Iran, Turkey, Russia and China.

Despite all efforts of Russia, China, Iran and other countries to shift away from US dollar dependence for international trade and finance, the dollar remains still unchallenged as world central bank reserve currency, some 63% of all BIS central bank reserves. Moreover almost 88% of daily foreign currency trades are in US dollars. Most all oil trade, gold and commodity trades are denominated in dollars. Since the Greek crisis in 2011 the Euro has not been a serious rival for reserve currency hegemony. Its share in reserves are about 20% today.

Since the 2008 financial crisis the dollar and the importance of the Fed have expanded to unprecedented levels. This is only now beginning to be appreciated as the world begins to feel for the first time since 2008 real dollar shortages, meaning a much higher cost to borrow more dollars to refinance old dollar debt. The peak for total emerging market dollar debt falling due comes in 2019, with more than 1.3 trillion dollars maturing.

Here comes the trap. The Fed is not only hinting it will raise US Fed funds rates more aggressively later this year into next. It is also reducing the amount of US Treasury debt it bought after the 2008 crisis, so-called QT or Quantitative Tightening.

From QE to QT…

After 2008 the Fed began what was called Quantitative Easing. The Fedbought a staggering sum of bonds from the banks up to a peak of 4.5 trillion dollars from only 900 billion dollars at the start of the crisis. Now the Fed announces it plans to reduce that by at least one third in coming months.

The result of QE was that the major banks behind the 2008 financial crisis were flooded with liquidity from the Fed and interest rates plunged to zero. That bank liquidity was in turn invested in any part of the world offering higher returns as US bonds paid near zero interest. It went into junk bonds in the shale oil sector, into a new US housing mini boom. Most markedly the liquid dollars went into higher-risk emerging markets like Turkey, Brazil, Argentina, Indonesia, India. Dollars flooded into China where the economy was booming. And the dollars poured into Russia before US sanctions earlier this year began to put a chill on foreign investors.

Now the Fed has begun QT – Quantitative Tightening – the reverse of QE. Late 2017 the Fed slowly began to shrink its bond holdings which reduces dollar liquidity in the banking system. In late 2014 the Fed already stopped buying new bonds from the market. The reduction of the bond holdings of the Fed in turn pushed interest rates higher. Until this summer, it was all “gently, gently.” Then the US President launched a global targeted trade war offensive, creating huge uncertainty in China, Latin America, Turkey and beyond, and new economic sanctions on Russia and Iran.

Today the Fed is allowing 40 billion dollars of its Treasury and corporate bonds mature without replacing them, rising to 50 billion dollars monthly later this year. That takes those dollars out of the banking system. In addition, to aggravate what is quickly becoming a full-blown dollar shortage, the Trump tax cut law is adding hundreds of billions to the deficit that the US Treasury will have to finance by issuing new bond debt. As the supply of US Treasury debt rises, the Treasury will be forced to pay higher interest to sell those bonds. Higher US interest rates already are acting as a magnet to suck dollars back into the US from around the world.

Adding to the global tightening, under pressure from the dominance of the Fed and the dollar, the Bank of Japan and the European Central Bank have been forced to announce they would no longer buy bonds in their respective QE actions. Since March, the world has de facto been in the new era of QT.

From here it looks to get dramatic unless the Federal Reserve does an about face and resumes with a new QE liquidity operation to avoid a global systemic crisis. At this juncture that looks unlikely. Today the world central banks more than even before 2008, dance to the tune played by the Federal Reserve. As Henry Kissinger allegedly stated in the 1970’s “If you control the money, you control the world.”

A 2019 New Global Crisis?

While so far the impact of dollar contraction has been gradual, it’s about to get dramatic. The combined G-3 central banks’ balance sheet increased by a mere 76 billion dollars in the first half of 2018, compared with a 703 billion dollars rise in the prior six months – almost half a trillion of dollars gone from the global lending pool. Bloomberg estimates that net asset purchases by the three main central banks will fall to zero by the end of this year, from close to 100 billion dollars a month at the end of 2017. Annually that translates into an equivalent 1.2 trillion dollars less of dollar liquidity in 2019 in the world.

The Turkish Lira has dropped by half since early this year in relation to the US dollar. That means Turkish large construction companies and others who were able to borrow “cheap” dollars, now must find double the sum of US dollars to service those debts.The debt is not state Turkish debt for the most part but private corporate borrowing. Turkish companies owe an estimated 300 billion dollars in foreign currency debt, most dollars, almost half the entire GDP of the country. That dollar liquidity has kept the Turkish economy growing since the 2008 US financial crisis. Not only the Turkish economy…Asian countries from Pakistan to South Korea, minus China, have borrowed an estimated 2.1 trillion dollars.

As long as the dollar depreciated against those currencies and the Fed kept interest rates low – as from 2008 – 2015, there was little problem. Now that’s all changing and dramatically so. The dollar is rising strongly against all other currencies, 7% this year. Combined with this, Washington is deliberately initiating trade wars, political provocations, unilateral breaking of the Iran treaty, new sanctions on Russia, Iran, North Korea, Venezuela, and unprecedented provocations against China. Trump’s trade wars, ironically, have led to a “flight to safety” out of emerging countries like Turkey or China to the US markets, most notably the stock market.

The Fed is weaponizing the US dollar and the preconditions are in many ways similar to that during the 1997 Asia crisis. Then all it needed was a concerted US hedge fund attack on the weakest Asian Tier economy, the Thai Baht to trigger collapse across most of South Asia to South Korea and even Hong Kong. Today the trigger is Trump and his bellicose tweets against Erdogan.

The US Trump trade wars, political sanctions and new tax laws, in the context of the clear Fed strategy of dollar tightening, provide the backdrop to wage a dollar war against key political opponents globally without ever having to declare war. All it took was a series of trade provocations against the huge China economy, political provocations against the Turkish government, new groundless sanctions against Russia, and banks from Paris to Milan to Frankfurt to New York and anyone else with dollar loans to higher risk emerging markets began the rush for the exit. The Lira collapses as a result of near panic selling, or the Irancurrency crisis, the fall of the Russian ruble. All reflects the beginning, as likely does the decline in the China Renminbi, of a global dollar shortage.

If Washington succeeds on November 4 in cutting all Iran oil exports, world (dollar) oil prices could soar above 100 dollars, adding dramatically to the developing world dollar shortage. This is war by other means. The Fed dollar strategy is acting now as a “silent weapon” for not so quiet wars. If it continues it could deal a serious setback to the growing independence of Eurasian countries around the China New Silk Road and the Russia-China-Iran alternative to the dollar system. The role of the dollar as lead global reserve currency and the ability of the Federal Reserve to control it, is a weapon of massive destruction and a strategic pillar of American superpower control. Are the nations of Eurasia or even the ECB ready to deal effectively?

F. William Engdahl is strategic risk consultant and lecturer, he holds a degree in politics from Princeton University and is a best-selling author on oil and geopolitics, exclusively for the online magazine “New Eastern Outlook.”

journal-neo.org/2018/08/20/washington-s-silent-weapon-for-not-so-quiet-wars/

|

|

|

|

Post by 3bid on Oct 5, 2018 1:32:26 GMT -5

The Collapse of the American Empire?

Published on Sep 12, 2018

The Agenda welcomes Pulitzer Prize-winning journalist Chris Hedges, who over the past decade and a half has made his name as a columnist, activist and author. He's been a vociferous public critic of presidents on both sides of the American political spectrum, and his latest book, 'America, the Farewell Tour,' is nothing short of a full-throated throttling of the political, social, and cultural state of his country.

|

|

|

|

Post by imSINGLEruRICH on Oct 9, 2018 13:25:42 GMT -5

Casualty Lists From the Kavanaugh Battle

October 9, 2018

Guest Post by Pat Buchanan

After a 50-year siege, the great strategic fortress of liberalism has fallen. With the elevation of Judge Brett Kavanaugh, the Supreme Court seems secure for constitutionalism — perhaps for decades.

The shrieks from the gallery of the Senate chamber as the vote came in on Saturday, and the sight of that bawling mob clawing at the doors of the Supreme Court as the new justice took his oath, confirm it.

The Democratic Party has sustained a historic defeat.

And the triumph is President Trump’s.

To unite the party whose nomination he had won, Donald Trump pledged to select his high court nominees from lists prepared by such judicial conservatives as the Federalist Society. He kept his word and, in the battle for Kavanaugh, he led from the front, even mocking the credibility of the primary accuser, Christine Blasey Ford.

Trump has achieved what every GOP president has hoped to do since the summer of ’68, when a small group of GOP senators, led by Bob Griffin of Michigan, frustrated and then foiled a LBJ-Earl Warren plot to elevate LBJ crony Abe Fortas to chief justice in order to keep a future President Nixon from naming Warren’s successor.

Sharing the honors with Trump is Majority Leader Mitch McConnell.

Throughout 2016, McConnell took heat for refusing to hold a hearing on Barack Obama’s nominee, Judge Merrick Garland, to fill the chair of Justice Antonin Scalia, who had died earlier that year.

In 2017, McConnell used Harry Reid’s “nuclear option” to end filibusters for Supreme Court nominations, and then got Judge Neil Gorsuch confirmed 54-45.

Last week, in one of the closest and most brutal court battles in Senate history, McConnell kept his troops united, losing only Sen. Lisa Murkowski, to put Kavanaugh on the court by 50-48. McConnell will enter the history books as the Senate architect of the recapture of the Supreme Court for constitutionalism.

This was a huge victory for conservatism and for the Republican Party. And the presence on the court of octogenarian liberals Ruth Bader Ginsburg and Stephen Breyer, both appointed by Bill Clinton, suggests that McConnell may have an opportunity to ensure the endurance of his great achievement.

The ferocity and ugliness of the attacks on Kavanaugh united Republicans to stand as one against what a savage Senate minority was trying to do to kill the nomination. And at battle’s end, the GOP is more energized than it has been all year for this fall’s election.

How united is the GOP? Conservatives are hailing the contributions of Sens. Jeff Flake, Lindsey Graham and Susan Collins, who delivered a masterful summation of the Kavanaugh case Saturday afternoon.

For the Democratic Party, the Kavanaugh battle was the Little Bighorn, as seen from General Custer’s point of view.

Unable to derail the judge during the regular confirmation process, they lay in the weeds until it was over, and then sandbagged the judge by leaking to The Washington Post a confidential letter Dr. Ford did not want released.

They thus forced a public hearing of charges of attempted rape against a nominee, demanded the FBI investigate all charges of sexual misconduct when Kavanaugh was a teenager, and ended up losing anyway.

Then the Dems watched protesters dishonor the Senate in which they serve by screaming from the gallery. It was among the lowest moments in the modern history of the Senate, and it was the Democratic minority that took it down to that depth.

Understandably, they are a bitter lot today.

And the #MeToo movement has been set back. For many of its champions were, in Kavanaugh’s case, demanding a suspension of the principle of “innocent until proven guilty,” and calling for the judge’s rejection in disgrace, based solely on their belief in a wholly uncorroborated 36-year-old story.

So where are we going now?

While Republicans are united and celebrating a great victory, the left and its media auxiliary are seething with rage and doubly determined to deliver payback in the elections four weeks away, where Democrats could pick up the two dozen seats needed to recapture the House.

Should they do so, however, they will face two years of frustration and failure. For the enactment of any major element of their liberal agenda — a $15 minimum wage, “Medicare-for-all” — would die in a Republican Senate, or in the Oval Office where it would face an inevitable veto by Trump.

So, what does 2019 look like, if Democrats capture the House?

Speaker Nancy Pelosi. A House Judiciary Committee headed by New York’s Jerrold Nadler who is already howling for impeachment hearings on both Kavanaugh and Trump.

And, by spring, a host of presidential candidates, none of whom looks terribly formidable, led by Cory (“I am Spartacus”) Booker, trooping through Iowa and New Hampshire, trashing President Trump (and each other), and offering themselves as the answer to America’s problems.

Bring it on!

www.theburningplatform.com/2018/10/09/casualty-lists-from-the-kavanaugh-battle/

|

|

|

|

Post by 3bid on Oct 26, 2018 9:47:24 GMT -5

Central Bankers Really Have No Idea What They're Doing with MoneyBy Jeffrey Snider

October 26, 2018

The ECB this week maintained its commitment to steadfast blindness. Don’t worry, they’ve done this before. Twice, actually. At least in 2018 they are only pledging to end what will be nearly four years of quantitative easing. There hasn’t been any easing, and given how QE has been changed along its trajectory it can’t have been too quantitative, either.

In 2011, believing similarly it had reached the end of its task Europe’s central bank exited then, too. Seven and a half years ago, officials voted for two successive benchmark rate increases, first in April and then again at the beginning of July. Mere weeks after the second, the world was in crisis again. Before the end of the year, Europe’s entire economy was in recession for a second time in three years.

Central bankers didn’t cause that contraction just as they hadn’t the first time. In July 2008, Europe’s Economists declared Europe free from overseas turmoil. The Americans were in trouble but even then it seemed, to Economists anyway, they would pull out of it before it went too far. The ECB raised its benchmark rate 25 bps to 4.25%.

Just as it would in 2011, in 2008 the institution ended the year going in the other direction. Officials were quick to declare the panic “unexpected” and therefore what could they do? One ECB Executive Board Member, Gertrude Tumpel-Gugerell, would attempt to explain ten years after the rate hike:

Balderdash. For one, what did Lehman have to do with euros? To answer that question honestly would mean seeing these central bankers for what they really are.

Markets are being reminded again in 2018 after, frustratingly, giving them the benefit of the doubt in 2017. There was some mild enthusiasm over globally synchronized growth, the idea that after a decade plus of stumbling around Economists had finally hit upon the right mix of policies to engineer full recovery at long last.

It was a preposterous idea given recent history. What were the chances, really, that after getting everything wrong for so long they would just get it right out of nowhere? Random good fortune, which the world holds in shorter supply than eurodollars these days, would have been the better bet.

In announcing his intention to end QE, ECB President Mario Draghi acknowledged this week, “incoming information, [is] somewhat weaker than expected” but that won’t deter the policy. Why would it? Draghi is merely returning to tradition, European officials who see an economy doing the very thing it isn’t.

There’s trouble in Germany, and if there’s trouble in Germany it will be worse elsewhere throughout the Continent. While Draghi was sounding petulant, that country’s IFO Centers for Economic Studies (CESIFO) released more troubling news. Sentiment weakened as conditions deteriorate, or “somewhat weaker than expected” if you prefer. Manufacturing assessments, in the aggregate, fell to the lowest since early 2017. Incoming orders declined for another month.

“Firms were less satisfied with their current business situation and less optimistic about the months ahead. Growing global uncertainty is increasingly taking its toll on the German economy.”

This follows closely another German economic survey, the ZEW, which worsened again also in September. Its Indicator of Economic Sentiment dropped back to -24.7, matching a multi-year low seen in July. The last time the ZEW was this bad on the way down was…August 2011.

If we look back at 2011 and 2008 what we find in both is the same “growing global uncertainty” as 2018. As yet, however, central bankers haven’t learned how to account for it, which is one reason why they don’t. In their view, Lehman was subprime mortgages and yet it was the final spark before full-blown worldwide panic and a global economic crash. Greece was supposedly the issue in 2011, but everywhere from China to Latin America to America the economy hasn’t yet recovered from it.

How did it get this way?

The answer is Paul Volcker. Mr. Volcker has been in the news, too, this week. Apparently in ill-health, the former Chairman of the Federal Reserve, the one before Alan Greenspan, Volcker has a lot to say. He told Andrew Ross Sorkin of The New York Times, “We’re in a hell of a mess in every direction.” It’s impossible to argue with him on that point.

“Respect for government, respect for the Supreme Court, respect for the president, it’s all gone. Even respect for the Federal Reserve.”

You can sense in his words great regret, a palpable degree of serious lament over how his predecessors at the Fed may have squandered his legacy. But what was his legacy really?

Volcker left the central bank in 1987 but wasn’t exactly a shoe-in to be reappointed in 1983 for a second four-year term. It was in his first stretch that made him the legend. One New York Times article written in March of ’83 on the topic of his uncertain reappointment ably summed up convention on Volcker.

“More important than theory is the fact that Mr. Volcker has come to be regarded as the helmsman who deserves most of the credit - blame, some say - for the tight-money policy the Fed pursued until last summer, a policy that brought on a deep recession that, in turn, slowed inflation from roughly 10 percent to 5 percent.”

He would come to be seen as the roaring eighties roared without the reemergence of the inflation monster as the man who single-handedly ended the Great Inflation. It would have been no small accomplishment, either, given that for fifteen years inflation was widely alleged as beyond anyone’s control.

Volcker would push short-term interest rates into double digits - twice. There were two recessions in the early part of the decade as a result, the second standing until 2008 as the worst since the Great Depression. His resolve in the face of unrelenting criticism was truly legendary. That much cannot be argued.

It was from this resolve that everything moved – a committed central bank could accomplish anything no matter what. The Federal Reserve itself would evolve as a consequence. It started the Great Inflation targeting money, and it ended it doing something altogether different. Because of the end of inflation, this different regime came to be regarded as the right choice.

As I have written about for years, in the tradition of a very few before me, the sixties and seventies were the period of “missing money.” If you are a central bank whose given mission is low unemployment and inflation, and intend to accomplish that mission naturally by targeting the money supply since inflation is a monetary phenomenon, missing money is an existential threat; which accurately and succinctly describes the Great Inflation.

If you can’t define money you certainly won’t be able to target it. Everything else falls into line from there. That includes the shift in monetary policy. Moving from Volcker forward, there wouldn’t be any money in it anymore. The Fed began to target other things simply because targeting money was, for them, impossible.

The global system (eurodollar) had begun to use exotic and undocumented transactional formats as money equivalents. Repo was a big one in those days, but tame now by 21st century standards. These were then expanded to offshore shadow spaces and expanded some more. Alan Greenspan would a quarter-century later only partially lament this “proliferation of products” before getting back on TV.

But if the central bank could no longer target money as it had done before, what did they do instead? Policymakers would shift beyond money into the real economy. What I mean by that is that they would take no notice whatsoever of the monetary system itself, the actual transactions in all their gory, incomprehensible details. In place of money they would stand to target a single interest rate.

By doing this, they set up what was essentially a default position. Banks operating in money markets would do whatever it is they wanted to do, and central bankers would take little or eventually no note of all that. Control would be removed from monetary cause and economic effect to working backward from economic effect.

It came to be believed that by doing so banks could define and use money in any way they saw fit, but all those hidden formats and uses would be governed in the aggregate by that single interest rate. When you step back and really appreciate what was attempted, it really is staggering conceit.

This requires a dramatic change in the way policy is made, too. When you target the money supply, you target the money supply. Forgive the tautology but it’s just that simple. You have to make judgements about the target, of course, but if the money supply starts to rise in relation there isn’t much thought about your response.

And that response is immediate.

In non-money monetary policy it is very different. Entering the economic process closer to the end than the monetary beginning, the central bank is forced into the future with its intentions. It has to rely on often far-out forecasts. It doesn’t know anything about money, therefore it is basing policy on the perceived results of what it doesn’t know.

In a simple system, if money becomes too plentiful we expect inflation to result. Under a money targeting system you don’t need to wait for the inflation to act; you stop the monetary growth before it ever gets that far.

But if you can’t define money and stop measuring for it, you have to predict inflation as it relates to other factors, often distant and indirect. It’s not so simple, and it puts the central bank in a huge bind. This method essentially trades monetary competence for the lust over forecasting skills. Thus, the unmovable infatuation with econometrics, especially of the neo-Keynesian variety (that doesn’t include the financial system as a modeled component).

I am oversimplifying here, but after Volcker in the early eighties this approach seemed to be corroborated by events. Consumer inflation stopped and the economy started to grow again without it. The so-called Great Moderation developed in the aftermath.

Without being able to define and measure money, however, there was no way to really be sure this evolution in monetary policy was responsible for it. Or whether it really was so moderate.

That’s why more than halfway into the Great “Moderation” many economists began to wonder what was really going on. The term itself was coined by a couple Ivy League Economists who, in the aftermath of the dot-com bust, were a little worried about being unable to explain exactly why everything was the way it was – and be able to tell if it would continue that way.

James Stock and Mark Watson in April 2002 would nervously conclude:

This was the real legacy of Volcker; determined monetary ignorance had left Economists unable to see or explain the very basis for the global economy. It wasn’t some minor, trivial matter to have puzzled over.

That much the world would confront just five years later. When faced with a problem in US subprime mortgages, Ben Bernanke, Volcker and Greenspan’s intellectual heir, was sublimely confident it was all a big nothing. European officials, too, which is why just two months before Lehman they were more concerned about their economy overheating. All of them relying on economic forecasts rather than being able to check those assumptions by close scrutiny of actual, effective monetary conditions.

But what is most scandalous of all is how this hasn’t been changed despite what happened ten years ago. Central bankers are still making forecasts from the same position of monetary ignorance, and thus they repeatedly get them wrong. They seek comfort in continuing to do things the way they’ve been doing them since Volcker, but they shouldn’t.

Many people have been betting that 2018 would be different. This time the forecasts (already trimmed down) would for once prove valid, they said. That’s always a possibility, but it would require more “good luck” than anyone has available.

Central bankers and Economists are sticking with their forecasts regardless. Draghi is matched and even exceeded in optimism by the Fed’s latest Chairman Jay Powell. Money markets, these eurodollar shadow spaces, are rendering them inoperable all over again. In one other development this week, the effective federal funds rate is now equal to IOER. They really have no idea what they are doing when it comes to money. And if they don’t know that, how can they have any idea about economy?

Just as Volcker was beginning his second term in 1984, former Treasury official Robert Roosa was very differently warning about:

Roosa did this at a conference in Bretton Woods sponsored by the Fed’s Boston branch.

What really happened in the early eighties, and this is the part most people have the greatest difficulty accepting, central bankers by losing touch with money let themselves become bystanders. They really believed they were in control of everything, and this what we’ve all been taught from Econ 101, by moving just the federal funds target around a little here and there. There was, in this detached view, no downside or detriment to knowing nothing about how anything was being funded (or where). It was all just myth and legend, beginning with Paul Volcker.

In the biggest ironic twist of them all, their continued forecast errors are predicated on this very myth. Every one of the central bank models simply assume that central banks aren’t really bystanders, which is why they never get them right.

The ECB’s rate hikes in 2008 and 2011 remind us of this uncomfortable truth. Europe’s central bank didn’t cause either crisis, for Europe or anywhere else, it merely went along for the ride completely helpless just like all the rest of them. Mario Draghi forecasts still good things ahead, but how would he know? It was Volcker who taught him and his compatriots they don’t have to.

This explains a lot about the last eleven years, and says even more about 2018.

www.realclearmarkets.com/articles/2018/10/26/central_bankers_really_have_no_idea_what_theyre_doing_with_money_103465.html

|

|

|

|

Post by 3bid on Nov 1, 2018 9:13:49 GMT -5

Why I think the Ugly October in Stocks Is Just a Preamble

by Wolf Richter • Oct 27, 2018

Yet, the crybabies on Wall Street are already clamoring for the “Powell put.”

Let me just say right up front: The stock market did not “collapse.” It has experienced a sell-off that made some people’s ears ring, as sell-offs normally do, and October has been ugly so far, but it wasn’t a “collapse.”

This matters because the crybabies on Wall Street are already clamoring for the “Powell put.” But the folks at the Fed have been around, and they know what a routine sell-off looks like and what a crash looks like, and they’re glancing at these numbers, and they yawn. Because in the grander scheme of things, not much has happened yet. The next uptick lurks around the corner, powered by the dip buyers and massive corporate share-buybacks.

After the dotcom bubble, the Nasdaq plunged 78%. Wave after wave of dip buyers were rewarded with small goodies and then taken out the back and shot. Many companies disappeared entirely. That was an example of a collapse. That’s when the Fed got nervous.

Today there are only some segments that have gotten hit very hard, though it’s still no collapse, and we’ll get to a few of them.

The Dow was well-behaved. It fell about 3% for the entire week and is about flat year-to-date. Nothing special. The Dow is only 8.4% off its peak. And compared to a year ago, it’s still up 5.4%.

It’s not a crime for stocks to be flat year-to-date. Stocks might actually be down for the year, and they might be down for years. But people have forgotten, and younger people have never experienced it in their life, after a decade of blatant market manipulations by central banks that have created this centrally planned Everything Bubble that is now “gradually” deflating.

The S&P 500 fell about 4% this week and is only 9.3% off its peak. It’s about flat year-to-date (well, down a minuscule 0.6%) and up 3% compared to a year ago.

The Nasdaq fell 3.8% in the week and is down 12% from its peak, nearly all of it in October. But it’s still up 3.8% year-to-date and up nearly 7% from a year ago. This is a far cry from being down 78%!

Fed Chairman Jerome Powell isn’t going to get rattled by these numbers. Young investors who’ve never seen a real sell-off might, but Powell is an old hand, and this sell-off overall is nothing yet, especially after the huge run-up. For real damage to occur, the trip south would have to take a long time – years! And we’re just looking at the beginning of it.

And the crybabies on Wall Street are just crybabies.

That said, it’s getting interesting in some sectors. And this too is typical for the beginning of a stock-market downturn: Some segments let go first, others follow. When story-segments lose their story, they plunge. It’s that simple. Here are a few examples:

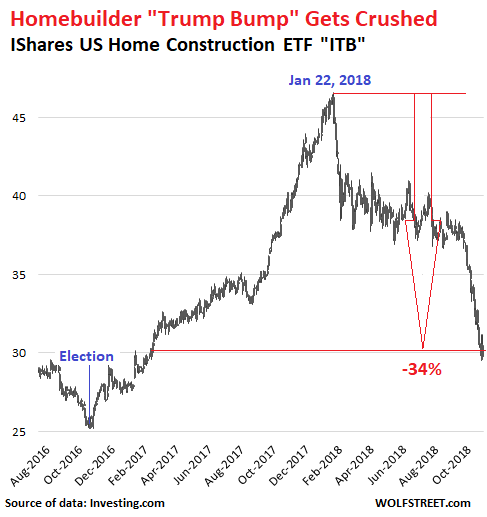

Homebuilders are getting crushed. Homebuilder stocks took off after the election in 2016, on a wing and a prayer, powered by hype about a Trump-inspired housing construction boom. The IShares US Home Construction ETF [ITB] soared 51% from November 3, 2016, through January 22, 2018.

But then reality set in that there would be no Trump-inspired housing construction boom, and that instead the housing market was beginning to hiss hot air. The ETF then plunged 34% over the nine months. Nearly the entire “Trump bump” has been wiped out even as the housing downturn has just begun (stock data via Investing.com):

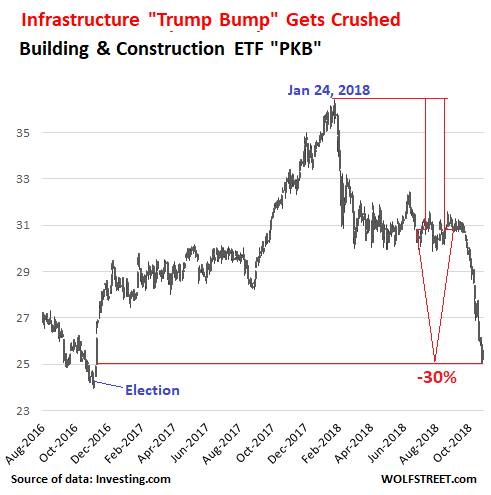

Building and Construction stocks surged 50% after the election in hopes for a mega construction boom, based on the story of a $1.5 trillion infrastructure plan. Much of that $1.5 trillion would be distributed to these companies, that was the hype. When markets realized that this plan was a head-fake, these stocks started to crash.

The PowerShares Dynamic Building & Construction ETF [PKB] has plunged 30% since January 23 and is back where it had been right after the election. This shows the “Trump bump” in operation: soaring on Wall-Street hype and crashing on reality:

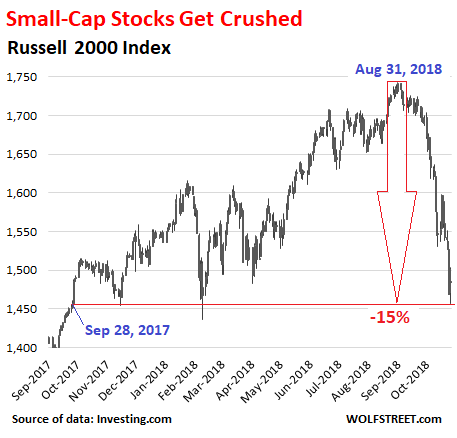

Small-cap stocks are letting go. The Russell 2000 index, which tracks the stocks with smaller market capitalization, has plunged 15% since August 31. These companies are heavily focused on US operations, unlike their big brethren that have large operations overseas. The index is now down year-over-year, and is back where it had been on September 28, 2017:

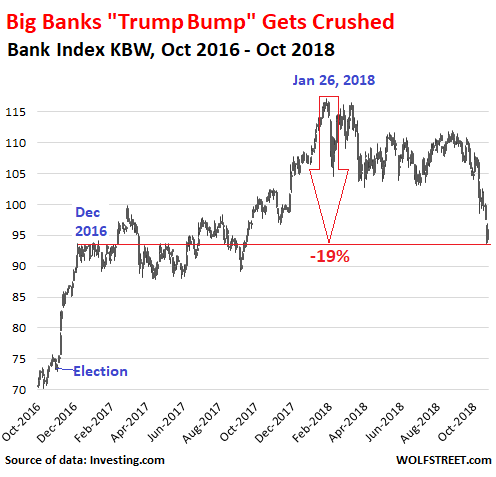

The Big Banks are losing it. The US KBW Bank index, which tracks large US banks, spiked after the election in November 2016 on hope – now being realized – of banking deregulation by the incoming administration, at the time being staffed with Wall-Streeters. Then these stocks floundered until late 2017. When the corporate tax cuts started becoming reality, the bank stocks surged again. From the election through January 26, the KBW Bank index soared 55%.

But that was the peak. The index has since plunged 19%, and is back where it had been in February 2017, or about 18 months ago, having unwound over half of the banks “Trump bump”:

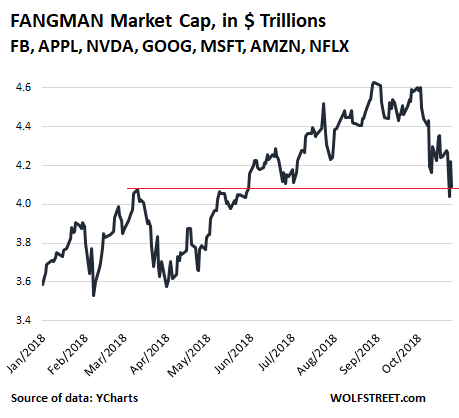

The FANGMAN stocks – Facebook, Amazon, Netflix, Google’s parent Alphabet, Microsoft, Apple, and NVIDIA – have lost $538 billion in market capitalization from their combined peak of $4.63 trillion on August 31. In other words, $538 billion went where it had come from.

But that 12% dive took them back to where they’d been on May 30. So, given the ludicrously ballooning share prices, nothing serious has happened yet. Remember: the entire Nasdaq plunged 78% over the years following the dotcom peak. And many stocks disappeared entirely.

Nevertheless, there was some variation: Apple [AAPL], the giant among giants, has dropped only 6.6% from the peak on October 3, and Microsoft [MSFT] only 6.9% over the same period. But Amazon [AMZN] has plunged 20% since September 4 and Facebook [FB] 33% since July 25.

So it boils down to this: Some stocks have gotten crushed, but the market overall has barely been dented – though the fundamentals are rotten, shares are still ludicrously overpriced, enthusiasm is still exuberant except on bad days, and blind faith in annually rising stock prices still reigns. And the fact that stocks like Tesla [TSLA] or Netflix continue to levitate beyond all reality shows that this downturn has a long way, and years, to go.

wolfstreet.com/2018/10/27/ugly-october-stocks-is-preamble-homebuilder-banks-construction-fangman/

|

|

|

|

Post by imSINGLEruRICH on Nov 5, 2018 18:13:27 GMT -5

|

|

|

|

Post by 3bid on Nov 11, 2018 10:41:00 GMT -5

American Mythology and the loss of democracy

Published on Jun 23, 2018

Ralph Nader, Consumer Advocate and former Presidential Candidate, discusses American Mythology with Chris Hedges.

www.youtube.com/watch?v=y9OJZOMEjOU

|

|

|

|

Post by 3bid on Dec 1, 2018 20:03:23 GMT -5

Chris Hedges - The American Empire Will Collapse Within a Decade, Two at Most

Published on Nov 20, 2018

Here, Chris speaks with CBC Radio about his new book and predicts that the US empire will collapse within the next 20 years, probably within the next 10.

|

|

|

|

Post by 3bid on Dec 4, 2018 13:06:01 GMT -5

Cannabis over oil?

Dec 03, 2018

A bust in the oil industry has some people feeling like the grass is greener on the other side. One company is selling off all its oil and gas assets to fully transition into becoming a cannabis producer.

|

|

|

|

Post by imSINGLEruRICH on Dec 12, 2018 21:48:56 GMT -5

Well good for Gem Oil & Rio Tinto........... <sigh> for us Uncle Melvin Wednesday, 12/12/18 12:17:30 PM Re: None 0 Post # of 352646 NEWS RELEASE

SASKATCHEWAN DIAMOND EXPLORATION

December 12, 2018 Gem Oil Inc. is pleased to announce Pioneer Aerial Surveys Ltd. of Flin Flon Manitoba has completed a drone geophysical survey over four kimberlites located in the FalCon Mining Camp of Saskatchewan near the villages of Weirdale and Smeaton all road accessible. The fourteen mining-claims totaling 2240 acres were acquired by staking in June 2017, are owned 100% by GEM. Saskatchewan Mineral Deposit Index 502 Kimberlite - www.economy.gov.sk.ca/dbsearch/MinDepositQuery/default.aspx?ID=2848 501 Kimberlite - www.economy.gov.sk.ca/dbsearch/MinDepositQuery/default.aspx?ID=2849 503 Kimberlite - www.economy.gov.sk.ca/dbsearch/MinDepositQuery/default.aspx?ID=2850 Carolyn Kimberlite - www.economy.gov.sk.ca/dbsearch/MinDepositQuery/default.aspx?ID=2863 The FalCon kimberlite field is the world’s largest cluster of kimberlites and has become a focus of world diamond interest due to the exploration-activities of Rio Tinto Exploration Canada, Inc. The Weirdale Kimberlites, 42 km northeast of Prince Albert, were discovered in 1989 by follow-up to an airborne magnetic survey by the FalCon Joint Venture of Uranerz Exploration and Mining Ltd. and Cameco Corp. The property contains two drill-indicated kimberlites and three other weak magnetic anomalies that may be indicative of smaller intrusive bodies. The margin of Kimberlite 501 was intersected by a ‘rotary air blast’ drill hole which cut 45 metres of kimberlite at a depth of 157 metres. Two drill holes were targeted on Kimberlite 502 – the first was a rotary drill hole which intersected kimberlite at a depth of 122.5 metres and was terminated at 140.2 metres because of drilling difficulty. The second drill test, in 1996, was a small diameter reverse-circulation hole which was terminated in kimberlite at a depth of 206 metres, again because of drilling difficulties. Based on a geophysical modeling of Kimberlite 501, a calculated area of 8.9 hectares of greater than 100 metre thickness at a depth of 125 metres (with a thinner “apron-type” crater facies kimberlite of 40-50 m thickness extending to the south, east and west covering an additional 26.1 ha). Kimberlite 502 has an estimated area of 7.1 hectares of greater than 100 m thickness at a depth of 120 m, with a 25 hectare ‘apron’ of kimberlite which is 40 to 60 m thick. Full vertical extent and the possibility of locating feeder pipes to Kimberlites 501 and 502 remain untested by drilling. Both kimberlites, with a total estimated volume 200 million tonnes, remain significantly under-tested in terms of sampling and diamond recovery. Only a small portion of the intercepts in the first two holes were tested for macrodiamonds (with negative results), and only 3 small selected samples (totaling 113 kg) from the last drill hole were tested for microdiamonds (1 stone recovered). Conclusions and Recommendations Insufficient and inefficient testing of the kimberlites makes it impossible to make any determination of the economic viability of the Weirdale and Smeaton kimberlites. Additional work to proceed in 2019. De Beers Canada, Inc. previously stated that modelled stone content of Kimberlite 141, based on their 2000 sampling, at 18 carats per hundred tons with a value of $153 US per carat, more than double the result of a previous bulk sample. Of note, De Beer’s comment the majority of the value is likely to occur as a consequence of a very coarse diamond size distribution – suggesting a potential stone population in the one to ten-carat range. On behalf of GEM OIL INC. Shaun Spelliscy, Managing Director GEMOIL actively exploring and developing mineral interests in Western Canada since 1957 www.gemoil.ca Uncle Melvin Wednesday, 12/12/18 08:14:01 PM Re: bigbadjohn post# 352632 0 Post # of 352646

Rio Tinto set to ramp up activity at Star Diamond site

December 12, 2018 07:13 am

By Glenn Hicks Rio Tinto says it’s too early to speculate on the long term viability of a proposed diamond project in the Forte à la Corne forest 60 kilometres east of Prince Albert. The company also stressed it’s too early to say what benefit or revenue-sharing arrangements may be possible with local Indigenous groups. The mining giant is now ramping up its community engagement ahead of large-scale exploration work for what the company labelled Project Falcon starting in the spring. After decades of talk and hope around the region, it appears the gears are starting to grind on a project that has the potential to provide 700 jobs and generate big revenue for the provincial coffers if it moves into full scale operation. The province confirmed the project’s environmental assessment approval in October. Rio Tinto general manager of exploration in North America Mark Tait spoke to paNOW as they await the winter thaw before proceeding with a series of 10 huge sample holes at the Star-Orion South site. While stressing it was still early days, Tait said the company sees an opportunity. “What I can point to is that we are certainly committed to the first phase of work, which is a significant investment, and we wouldn’t be doing that if we didn’t see potential in the project,” he said. This initial exploration phase is an $18 million investment that will include the trench-cutting sampling work, and an on-site processing plant among other activities. That will mean jobs through the company’s regular contractors in both heavy machinery opportunities and the running of the work camp such as catering. The company has a deal with the property owners Star Diamond to spend up to $80 million on the life of the project over a multi-phase approach that could see them acquire a 60 per cent stake in the venture. The mine could operate for over 30 years and extract billions of dollars in diamonds, according to previous initial analyses. Could Indigenous groups see benefit arrangements? The James Smith Cree Nation (JSCN), whose land is adjacent to the proposed mine, has rejected the project at it stands. Members state the damage caused to the forest by mining operations would be far greater than what was initially portrayed and there would be “significant unmitigated impacts.” The First Nation said it wanted real benefits from the project such as revenue-sharing. Tait said it was too early to say what a future mine site might look like and how the mining would impact environmental values. “We’re focused on exploring and evaluating the ore body,” Tait said. “We’re a long way from determining what a mine plan and broader impact on the project area might look like. We’re still in a stage where we don’t have any ownership of the project for us to speculate around what future IBA (Impact and Benefits Agreement) or revenue-sharing arrangements would look like, it’s too early for us to say.” Tait did stress Rio Tinto worked with other Indigenous groups globally but said it was too early to go into specifics on what could or couldn’t happen at Project Falcon. The provincial government has already made it clear they do not enter into such arrangements on proposals like this. JSCN has previously stated its confidence in Rio Tinto’s involvement because of their “maturity” in social and environmental responsibility. Tait said they had had various meetings with local organizations and groups including one-on-one time with the JSCN and the Métis Nation. He said members of the First Nation went on a tour of the exploration site and the company was well aware of what the project meant for the local environment. “Our exploration activities are conducted globally in both an environmentally and socially responsible manner,” he said. “We engage with communities right up front. They can come and see what we’re doing, understand what the work looks like, and how it may or may not impact on the broader environment.” Tait added they can demonstrate when they finish their activities that they “make a significant effort to reclaim those areas to the standards required.” Advisory committee to communicate timely information as project progresses With a ramping-up of activities in the coming months, Tait couldn’t say how many jobs would become available, but said further outreach with communities and open houses would be scheduled. He encouraged anyone with questions, comments or feedback to contact their local member of the Diamond Development Advisory Committee (DDAC), which has representation from many local community groups. People can also contact cp Julia Ewing, a community relations consultant at julia.ewing@sasktel.net. Rio Tinto said the committee was there so they could take local interests into account, including opportunities for local employment and procurement. |

|

|

|

Post by 3bid on Jan 5, 2019 15:41:44 GMT -5

NEO: Death of Democracy, America’s Loss of Rule of LawBy Gordon Duff, Senior Editor - January 5, 2019 By Gordon Duff and New Eastern Outlook, Moscow As of the beginning of 2019, America enters a meltdown. Congress, under the House leadership of Nancy Pelosi, says President Trump may well be indicted for crimes, election fraud, conspiracy, obstruction of justice, tax evasion, no one is sure except maybe Special Counsel Robert Mueller. What is known, however, is that the deterioration of rule of law in the US has gone on for decades with the scales of justice under the absolute control of the powerful and corrupt. What is also know to anyone who pays remote attention is that it is the GOP, which doesn’t necessarily mean Donald Trump, that has been bought and paid for by special interests. This issue has come to light only recently, and to a degree few are aware, as moves unseen by the public are bringing potential reforms into play. The powerbases within the military and intelligence community, never well understood and too often assumed to be owned by Israel or Wall Street, are close to quietly assuming power. Past that, business leaders are also organizing, terrified of runaway policies that have led to even deeper debt, potential civil unrest and, most threatening of all, the collapse of the dollar. Even less well known are groups that have long recognized and opposed the Deep State, even when it was called “the Illuminati” or “Bilderbergers” or whatever the flavor of the month term may have been. The enemies of entropy, some now with potential billions of dollars in backing, stand ready to issue a secret ultimatum to Donald Trump. Trump is the “wild card,” neither “goose nor gander.” Behind his visible gross incompetence and outrageous behavior are occasional acts of defiance that may be accidental or may be utter brilliance, no one really knows. Be that as it may, the only way America can be saved, not just through newfound isolationism or trade wars, is through restoration of traditional checks and balances that long ago melted away as the fake “conservative right” reengineered America’s institutions to fail. America was never intended to be a democracy. With a population of immigrants, many incredibly poor and uneducated, any political con man, like perhaps Donald Trump, if the example fits, could hoodwink Americans into political suicide. America under her current constitution wasn’t really founded by “Founding Fathers,” but rather by those who came by later, opportunists, speculators and too many with strong ties to secret societies and European banks, if historian Charles A. Beard is to be believed as expressed in his 1913 seminal work, An Economic Interpretation of the United States. From Wikipedia, a weak but usable interpretation though wrought with the usual error that infects all Wikipedia works: “An Economic Interpretation of the Constitution of the United States argues that the structure of the [Constitution of the United States] was motivated primarily by the personal financial interests of the Founding Fathers; Beard contends that the authors of [The Federalist Papers] represented an interest group themselves. More specifically, Beard contends that the Constitutional Convention was attended by, and the Constitution was therefore written by, a “cohesive” elite seeking to protect its personal property (especially federal bonds) and economic standing. Beard examined the occupations and property holdings of the members of the convention from tax and census records, contemporaneous news accounts, and biographical sources, demonstrating the degree to which each stood to benefit from various Constitutional provisions. Beard pointed out, for example, that George Washington was the wealthiest landowner in the country, and had provided significant funding towards the Revolution. Beard traces the Constitutional guarantee that the newly formed nation would pay its debts to the desire of Washington and similarly situated lenders to have their costs refunded. Put into more modern terms for understandability, moves toward reforming term limits for congress, removing corporate and foreign cash from elections, reforming electoral districts, reforming the committee system in congress itself, these and more are needed to restore a semblance of representative government to America. Simply put, even with congress totally restructured, the runaway Supreme Court would require disbanding as well, it is a total failure, a “star chamber” owned by organized crime. Other institutions, let’s look at the courts. Money owns America’s courts and the rich appoint the judges, at least most of the time. Trump’s own appointments are 100% corrupt, a reason, a very good reason, to be suspicious of Trump’s real intent. From day one, Trump has backed powerful special interests that victimize Americans, pollution, dangerous foods, untested and overpriced drugs, financial scams and wholesale robbery of the US Treasury by “insiders” who contribute to right wing candidates. The evidence here is overwhelming. But courts are more than lawsuits and judges who protect criminals who victimize investors and consumers. Courts send people to prison. Toward that end America’s legal system is among the world’s worse. No one really knows how many Americans are in prison or under lessened freedom due to court findings, as many as 13 million some sources say. From a University of Georgia 2010 study: “Because the U.S. does not maintain a registry of data on people with felony convictions, researchers calculated estimates based on year-by-year data and used demographic methods to estimate the numbers of deaths and re-incarceration to establish a number for each state and year. The study estimates that as of 2010 there were 19 million people in the U.S. that have a felony record, including those who have been to prison, jail or on felony probation. Maps in the study illustrate the combined felony populations by state as of 2010, because states vary in their criminal justice policies, especially in how law enforcement, incarceration and community supervision are emphasized. States use different policy levers to decide how to sentence people, Shannon said. For example, Georgia and Minnesota have high rates of people on felony probation, though Minnesota is a low incarceration state. Georgia leads the nation in rates of probation. ‘In our communities all over the country people are living, working, paying taxes, or otherwise getting by all while facing the consequences of criminal justice experience that limit their life chances and also have spillover effects into our other social institutions,’ Shannon said.” Simply put, America puts people in prison, often prisons owned by corporations, corporations that pay to elect politicians that pass more and more laws criminalizing everything imaginable and promoting longer and longer prison sentences for anyone except, of course, the most dangerous “white collar” criminals of all, the members of congress themselves. Another institution is the press, hardly free, each year the “fake news” as Trump calls it, falls under more and more censorship or corporate ownership, which is one and the same. Where independent news may once have been seen as “conspiracy theory,” recent observation has shown that the internet monstrosities, Google and Facebook, with YouTube, Twitter and service providers onboard, are the real control of an unending and totally pervasive flow of rigged and fabricated information custom tailored to confuse and victimize. Past that, the traditional media is simply along for the ride, making it all up, seeing vast financial incentives in “dumbing down” America. With a system rigged to fail, corrupt police, jails for profit, fake news, fake history and a government that answers only to itself, the rule of law is less than even a memory. If the rule of law is to be restored, how much will the “powers that be” fight back? Are we describing civil war? Gordon Duff is a Marine combat veteran of the Vietnam War that has worked on veterans and POW issues for decades and consulted with governments challenged by security issues. He’s a senior editor and chairman of the board of Veterans Today, especially for the online magazine “ New Eastern Outlook.” journal-neo.org/2019/01/05/death-of-democracy-america-s-loss-of-rule-of-law/www.veteranstoday.com/2019/01/05/neo-death-of-democracy-americas-loss-of-rule-of-law/

|

|