|

|

Post by bunnyb on Aug 29, 2019 8:09:05 GMT -5

patrose!

Or should I say 'Lucy'?

F you and your football ,I am not going to try to kick it!

There is NEVER a ball where they say there is a ball.

The psychiatrist is in. Great racket drive them crazy then set up shop.

NO THANK YOU.

|

|

|

|

Post by 3bid on Sept 4, 2019 13:24:14 GMT -5

"The End Is Unforeseeable" - Negative Interest Rates Threaten The Entire Financial System

by Tyler Durden

Wed, 09/04/2019

Authored by Jim Bianco, op-ed via Bloomberg.com,

Former Federal Reserve Chairman Alan Greenspan recently said he wouldn’t be surprised if yields on U.S. bonds turned negative and if they do, it wouldn’t be “that big of a deal.”

That seems to be a sentiment widely held in central banking circles these days, but it’s wrong. Negative interest rates represent a threat to the financial system.

To understand why, let’s start with the existing fractional reserve banking system, which is more than a century old. For every dollar that goes into a bank, some set amount (usually about 10%) must go into a reserve account to be overseen by the central bank. The rest is either lent out or used to buy securities.

In other words, the fractional reserve banking system is leveraged to interest rates. This works when rates are positive. Loans are made and securities bought because they will generate income for the bank. In a negative rate environment, the bank must pay to hold loans and securities. In other words, banks would be punished for providing credit, which is the lifeblood of an economy. As German bankers recently explained to the European Central Bank:

We already have a devastating interest rate situation today, the end of which is unforeseeable,” Peter Schneider, who represents public-sector savings banks in the southern German state of Baden-Wuerttemberg, said on Wednesday. “If the ECB aggravates this course, that would hit not only the entire financial sector hard, but especially savers.

And to make matters worse, the German government is considering outlawing negative deposit rates. In a negative rate world, forcing rates on short-dated debt to zero would keep the yield curve permanently inverted. The fractional reserve banking system cannot operate properly in this environment.

Valuation models are another area of finance that need to be tweaked in a negative rate environment. Nobel prizes have been awarded to economists that developed concepts such as the efficient frontier, the Capital Asset Pricing Model and the Black-Scholes option pricing model. But when a negative value is assumed for the risk-free rate in these types of models, fair value results shoot off toward infinity. With trillions of securities and derivatives dependent on these models, valuation is critical.

In a similar vein, pensions use a discount interest rate to determine if they are properly funded. If one plugs in a negative interest rate as the discount rate, all pensions would technically be underfunded. The only pensions that would be properly funded would be those with assets exceeding expected liabilities. No pension is set up this way. Negative rates on fixed-income securities also means there is no way pension funds can ever generate enough income to meet their obligations.

When repurchase, or repo, rates go negative, lenders of securities must pay rather than receive income. Why would anyone lend out their securities if they also must pay for the privilege of doing so? Repos are the basic plumbing of the financial system, enabling the trade and settlement of securities transactions. If this market becomes dysfunctional, it is akin to the pipes in your walls leaking.

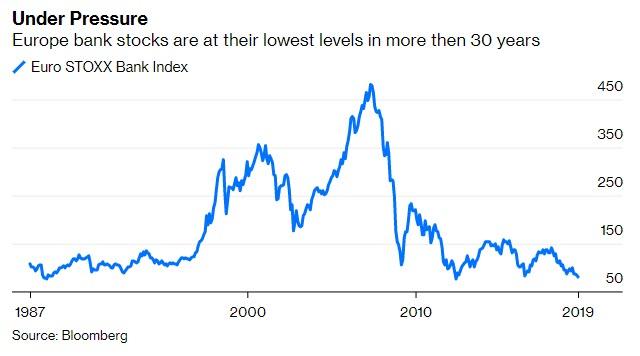

To see the results of low or negative rate environments, look no further than the euro zone and Japan. They account for 87% of the negative rates worldwide. Europe is essentially in recession with negative GDP in Italy, Germany and elsewhere. Its banking system is a mess, thanks to negative rates. As the chart below shows, European banks are trading at the lowest levels in more than 30 years.

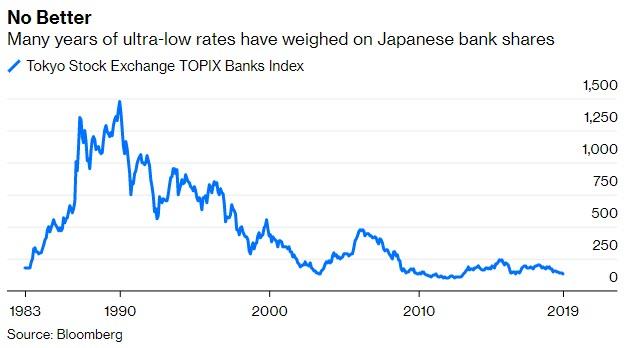

Japan is not doing much better. Economists are projecting negative GDP in the fourth quarter and the Japanese banking system is even worse than Europe’s, trading at some of the lowest since the early 1980s.

These are not isolated occurrences. The first instances of modern negative interest rates arrived in Switzerland in the 1970s. As Bloomberg Opinion Columnist Stephen Mihm recently detailed, the results were not pretty.

The U.S., UK, Canada, Australia and New Zealand are the only developed bond markets that do not have negative rates anywhere on their yield curves. Should these countries join the rest of the developed world in moving to negative rates, the financial system will be under much more stress. If negative rates become more widespread across the globe, then the financial system needs to be rebuilt on a new set of assumptions. The problem is we do not yet know what those should be or how they would work.

..........................

www.zerohedge.com/news/2019-09-04/end-unforeseeable-negative-interest-rates-threaten-entire-financial-system

|

|

|

|

Post by 3bid on Sept 10, 2019 18:50:56 GMT -5

The Collapse of the American Empire

America: The Farewell Tour

By John Allen | September 10, 2019 | Veterans Today

Chris Hedges’s profound and unsettling examination of America in crisis is “an exceedingly…provocative book, certain to arouse controversy, but offering a point of view that needs to be heard” (Booklist), about how bitter hopelessness and malaise have resulted in a culture of sadism and hate.

America, says Pulitzer Prize–winning reporter Chris Hedges, is convulsed by an array of pathologies that have arisen out of profound hopelessness, bitter despair, and a civil society that has ceased to function. The opioid crisis; the retreat into gambling to cope with economic distress; the pornification of culture; the rise of magical thinking; the celebration of sadism, hate, and plagues of suicides are the physical manifestations of a society that is being ravaged by corporate pillage and a failed democracy. As our society unravels, we also face global upheaval caused by catastrophic climate change. All these ills presage a frightening reconfiguration of the nation and the planet.

Donald Trump rode this disenchantment to power. In his “forceful and direct” (Publishers Weekly) America: The Farewell Tour, Hedges argues that neither political party, now captured by corporate power, addresses the systemic problem. Until our corporate coup d’état is reversed these diseases will grow and ravage the country. “With sharply observed detail, Hedges writes a requiem for the American dream” (Kirkus Reviews) and seeks to jolt us out of our complacency while there is still time.

|

|

|

|

Post by bunnyb on Sept 11, 2019 9:36:30 GMT -5

www.chicagotribune.com/nation-world/ct-nw-epstein-court-documents-unsealed-20190810-cju46mmxrfdypj3sscjyqbozb4-story.htmlIf you cannot capture all of them at least get rid of the heroic and patriotic ones through disaster and war. The remaining 'flock' will be less likely to protest being enslaved. Especially if you make them government dependent by wrecking the economy and addicting them to drugs and video games while taking away the freedom of speech and the right to bear arms. This is why we have no one left to fight, even by vote. Now more than ever, hero's always needed, but we may have run out.... I just had to repeat this here, it is relative to the post. Heroes are the vital component in any story line as are villains. The story would not be a complete one without either. A story requires a villain to be overcome and a hero to stand up to insurmountable odds do the right thing at great personal cost to defeat the villain. Then we get to the happy ending. If by some chance the hero does not stand up and do the right thing the villain wins and the story ends, badly. These type of stories always have a 'to be continued ' at the end. I hate that. Patterns repeat all stories are just a continuous repetition of the same pattern. Not just in fiction either, fiction is just a way to express a VERY REAL constant that is part of existence that cannot be denied. To deny that we need heroes is as impractical as the denial that we need our hearts to continue to beat to stay alive. I do not understand the forces that have prescribed the patterns of existence, but there is no denying the patterns are there, will continue, and will repeat. Call it Gods will, karma, or just the universe playing with us I DO NOT KNOW. But life, death, heroes, villains, good and evil all are part of the patterns that repeat. Ours is not to question why, ours is but to do or die. Heroes required.

|

|

|

|

Post by 3bid on Sept 13, 2019 18:06:23 GMT -5

$400 TRILLION HOLE? Actual US debt may be 2,000% of GDP, says Wall Street report

Published time: 12 Sep, 2019|RT

A new report suggests that the real US debt level may be $400 trillion, or 20 times higher than the country’s gross domestic product. The calculation includes government, state, local, financial and so-called entitlement debt.

AB Bernstein, a global asset management firm based on Wall Street, came up with these figures by including in its analysis not only traditional levels of public debt, such as bonds, but also financial debt as well as future obligations for entitlement programs. These include social security, Medicare and public pensions.

In its report, AB Bernstein took debt from a number of sources and compared it to GDP. Using this methodology, federal, state and local government debt combined amounted to 100 percent of GDP. Households and firms accounted for 150 percent, while debt held by financial firms came to 450 percent. Another 27 percent came from trusts for social insurance programs, 484 percent from promises under current social insurance programs, and 633 percent from obligations for social programs. The total debt therefore amounted to 1,832 percent.

“US debt is large. And it’s growing. But if we want to think about debt problems (in any sector – sovereign, households, firms or financials), the conditions rather than the levels are more significant,” Philipp Carlsson-Szlezak, chief US economist at AB Bernstein, said in the report.

It suggests that, although the figures seem depressingly large, it is important to understand that not all of the debt obligations are concrete, and there may be leeway. This is especially true for the government programs, which form the biggest potential debt but can be changed by legislation or accounting.

While the picture is dire, such numbers don’t prove we are doomed or that a debt crisis is inevitable.

“Debt problems could, arguably would have, already happened at lower levels of debt if the macro conditions forced it,” Carlsson-Szlezak noted. He also explained that crisis measures work both ways. An apparently smaller level of debt can cause major problems at a time when the economy is at its weakest, for instance in a financial crisis. At the same time, larger levels of debt can be harmless if other conditions, for example leverage levels, or debt to capital, are sustainable.

The total federal outstanding US debt has recently jumped to $22.5 trillion, or about 106 percent of GDP, CNBC reported. Without the intergovernmental obligations, debt held by the public amounts to $16.7 trillion, or 78 percent of GDP.

Carlsson-Szlezak noted in the report, however, that different debt carries different risks and its impact on individual parts of the economy would vary.

“A default on US treasury bonds would be catastrophic to the global economy – whereas changes in policy (while painful for those whose future benefits were diminished) would barely register on the economic horizon,” he stated.

....................

www.rt.com/business/468658-us-debt-report-economy/

|

|

|

|

Post by 3bid on Sept 17, 2019 15:34:26 GMT -5

NEO – Will the IMF, FED, negative interest and digital money kill the Western economy?

THE LATEST BANKING FRAUD HAS THE POOR FINANCING THE RICH VIA NEGATIVE INTEREST, which we have already, and steals money from depositors to give to large borrowers - a reverse cross-subsidy

By Jim W. Dean, Managing Editor

-

September 17, 2019 | Veterans Today

by Peter Koenig, …with New Eastern Outlook, Moscow

[ Editor’s Note: The “negative interest” issue seemed like a complicated one, as just the sound of it seemed counterproductive. For instance, “how could negative interest be paid, or accounted for?” Hence, I have stayed away from taking it on, waiting for someone else to dive into the topic.

NEO’s writers pool has a deep bench, and VT cherry picks what we feel our readers would like the most. Peter Koenig has the best piece on the topic I have seen so far. He cuts right to the chase:

“Negative interest, we have it already – it’s the latest banking fraud, stealing money from depositors to give to large borrowers. It’s a reverse cross-subsidy, the poor financing the rich. That’s the essence.”

I had of course suspected it was some kind of a book-juggling tool, to make things look better than they were, to hide a future reckoning day until after the retirement of those in charge now, so they do not have to explain what happened.

I would copy and paste this article into a file to keep for future reading, as we all need to get up to speed, not only learning the details of what is going on but also how to find a simple way to explain it to others; or else, most folks will miss what is going on completely.

It never ends. If they can’t get you one way, they get you another way… Jim W. Dean ]

Real money

– First published … September 15, 2019 –

The IMF, has been instrumental in helping destroying the economy of a myriad of countries, notably, and to start with, the new Russia after the fall of the Soviet Union, Greece, Ukraine and lately Argentina, to mention just a few.

Madame Christine Lagarde, as chief of the IMF had a heavy hand in the annihilation of at least the last three mentioned. She is now taking over the Presidency of the European Central Bank (ECB). There, she expects to complete the job that Mario Draghi had started but was not quite able to finish: Further bleeding the economy of Europe, especially southern Europe into anemia.

Let’s see what we may have in store – to come.

Negative interest, we have it already – it’s the latest banking fraud, stealing money from depositors to give to large borrowers. It’s a reverse cross-subsidy, the poor financing the rich. That’s the essence. It’s a new form of moving money from the bottom to the top. Now, a Danish bank has launched the world’s first negative interest rate mortgage.

It provides mortgages to home owners for a negative rate of 0.5%. The bank pays borrowers to take some money off their books. Of course, as usual, only relatively well-off people can become home owners and benefit from this reverse cross-subsidy. It is a token gesture, duping the public at large into believing that they are benefiting from the new banking stint. The bulk of such operations serve large corporations. The borrower pays back less than the full loan amount.

Switzerland may soon go into the direction of Denmark. Bank deposits with the central banks pay negative interest almost everywhere in the western world, except in the US – yet. It’s only a question of time until the average consumer will have to reimburse the banks for their central bank deposit expenses, meaning, the customers are getting negative interest on their deposits. That’s inflation camouflage.

A sheer fraud, but all made legal by a system that runs amok, that does not follow any ethics or legal standards. A totally deregulated western private banking system, compliments of the 1990s Clinton Administration, and, of course, his handlers.

As Professor Michael Hudson calls it, financial barbarism. We are haplessly enslaved in this aberrant ever more abusive private – fiat money – banking shenaniganism. RT’s Max Keiser recently interviewed Karl Denninger of Market-Ticker.org. Denninger told Keiser,

“Negative yielding bond is forced inflationary instrument: you buy it, you’re guaranteed inflation in the amount of a negative yield.” He blasted the tool as plain “theft” by any government that issues these bonds, which is done in an effort to nominally expand a country’s GDP. “If the government is issuing more in sovereign debt their GDP is expanding in nominal terms. If you have negative interest rates on those government bonds, you’re creating excess space for the government to run the fiscal deficit […] in excess of GDP expansion. Nobody in any civilized nation should allow this to happen because it is theft, on the scale of that differential, from everybody in the economy,”

To make sure the little saver doesn’t think about depositing his savings under his mattress or in a hole in the ground instead of bringing it to the bank, money will be digitized and cash will disappear. Madame Lagarde has already more than hinted at that, when she gave a pre-departure speech at the IMF – explaining on how she sees the future of monetary banking.

The future, according to her, being no more than 15 to 20 years away, is a no-cash society. Just enough time for the elder generations – those that may still feel an instinct of rejection and have some consciousness about personal privacy, those that may resist money digitization – may have died out. The young, up-and-coming age groups may be brainwashed enough to find a cashless society so cool.

Since Madame Lagarde is moving to head the ECB in Frankfurt, it is fair to assume that Europe will be one of the largest test grounds for digitized money, i.e. towards a cashless society. In fact, it is already a test ground – many department stores and other shops in Nordic countries – Sweden, Norway, Denmark, Finland – do no longer accept cash, only electronic money. In Denmark already up of 80% of all monetary transactions are made digitally.

Imagine, for your chewing gum wrapper, pack of cigarette, or candy bar, you swipe a card in front of an electronic eye – and bingo, you have paid, not touching any money – “that’s mega cool!”

That’s what the young people may think, oblivious to leaving a trail of personal data behind, among them their bank account details, their GPS-geared location, what they are shopping, a pattern of data that is in ten years-time expected to amount to about 70,000 points of information about an individual’s characteristics, emotions, preferences, photos, personal contacts… what Cambridge Analytica in the superb documentary “The Great Hack” revealed as already today on average 5,000 points of data per citizen.

The system will know you inside out better than you know yourself. And you will be exposed to algorithms that know exactly how to influence every action, every move of yours. Cool!

***

A horrendous trial on how an entire country, India, with the world’s second largest population, may react to demonization, was introduced in 2016 by President Modi, bending to the pressure of the western financial system, with support of the IMF and implementation funding by USAID.

It amounted in a disastrous and cruel demonetization, invalidating almost over-night the most popular 100 Rupee (Rs) bank note, replacing it with a 200 Rs note – which in most places, especially in rural towns, where banks are scarce, was not available. Never mind that less than half of the Indian population has a bank account where the bank note exchange transactions had to be carried out.

The sudden disappearance of the most popular bank note – more than 80% of all monetary cash transactions in India took place in 100 Rs notes – was a proxy to digitization of money. Countless people starved to death especially in rural areas, because their 100 Rs were declared worthless and became unacceptable to buy food.

***

The 340,000 citizens of Iceland have already a fully digitized e-ID, now moving towards a mobile ID, i.e. accessible through your smart phone – uniting every possible data that belongs to you, from medical records to insurance policies, all the way to dog, cat and car registrations – you name it.

Most say they trust their government and are not unhappy with their divulging their most intimate data. Many have no or little idea, though, to what extent the private sector is involved in setting up such a hermetic countrywide data bank for the government. – Even if the regulator is within then government and you trust your government, how much can you trust the profit-oriented private sector in protecting your data?

The surveillance state that you, among other clandestine intrusions into your privacy, will allow by willy-nilly accepting digitization of money, and eventually digitization of your entire private data, pales Orwell’s imagination of “1984”. Every citizen is registered in every western “security agency’s” electronic data bank – and of course those of the empire and Middle East affiliate, Israel, CIA, NSA, FBI, Mossad – and so on – no escaping anymore.

It just so happens that you, dear citizen, are oblivious to all of what is going on behind your back, since your attention will be captured by massive marketing and directed towards the nefarious machinations of the corporate elite ruled, globalized world, making you an eternal and ever-more intense consumer.

You must spend the last penny of your income on trendy stuff, all those fashion things that will be pumped non-stop day-in-day-out into your brain, what’s left of it, by propaganda on television, radio, electronic cartoon-like billboards, internet – and that at every turn you take. And let’s not forget sports events – they increase every year and are the most direct deviation tactic take-over from the Roman Empire.

The most aberrant trends will be cool, like shredded jeans, for which you pay a premium, body-paintings, called tattoos, footballer hair styles, because they are fashionable and your looks are key to fit into a standardized, globalized society that has seized thinking for itself – no more interest in politics, in what your non-democratically elected representatives decide for you. It’s what Noam Chomsky calls the marginalization of the populace.

You are made believe that you are living in a democracy where you can do what you want, shop what you want, watch what you want, and even when the elections or occasional referenda are offered to request your opinions, you are cheated into believing your choice is free.

Of course, it is not. It is all programmed. Algorithms drawing on your profile of 70,000 points of information on emotions, desires and dreams, will clandestinely help the ‘system’ to enslave, cheat and master you – and you won’t even notice.

That’s where we are headed, largely thanks to digitalization of money – but not only, because surveillance will also follow all your steps on internet, on Facebook, Twitter, Instagram, Whatsapp – and many more of those especially created marketing tools, implanted in societies’ social media, that make life and communication so much easier.

And there is more to digital money. Much more. In 2014, the unelected European Commission (EC) has put on its books of regulations, following a similar decree in the US, the rule that an overextended bankrupt too-big-to-fail private bank will no longer be rescued by the state, by your tax money – which used to be called a “bail-out”.

Instead, there will be “bail-ins”, meaning that the bank will seize your deposits, your savings and sanitize itself with money stolen from you. You have no choice, there will be no ‘run on the banks’ – because there is no cash to withdraw.

We have seen signs of this when Greece collapsed after 2010, and cash machines spitting out no more than 20 € per day – if at all. For many of Greek citizens – especially the poorer class living from day to day – this meant often cruel starvation.

Bail-ins are little talked about, but they happen already today and ever more so. In 2014, the Austrian bank Hypo Alpe Adria – the Heta Asset Resolution AG, was given green light by the Austrian Banking Regulator, the Austrian Financial Market Authority (FMA), to refinance itself by a so-called “haircut” of an average 54%, meaning, stealing 54% of depositors’ money.

But the first and largest “haircut” test took place in Cyprus, when in 2013 the Bank of Cyprus depositors lost about 47.5% in a “haircut” to bail out their bank. Of course, the big sharks were forewarned, so they could withdraw their money in time and transfer it abroad.

It could get worse. The state, tax authority, an institution, a corporation says you owe them money which you deny, possibly for a good reason – but they have access to your bank account and just seize the amount they pretend is their due. You are powerless against these tyrannical monsters and may have to hire expensive legal service to get your stolen money back – if at all.

Because the “system” is run by the “system”. And once that level has been reached, a form of Full Spectrum Dominance, a key target of the PNAC (Plan for a New American Century), there is hardly any escaping. That has all happened already, in front of our publicity-blinded eyes, little spoken about, the trend is growing – and this even without necessarily a digitized world.

Is it that the kind of society you want?

***

Then there are the rather prominent gurus who bet on gold and bitcoins to replace the faltering dollar, like a last-ditch solution. None of them is any more viable than the fiat dollar. Gold is highly volatile due to its vulnerability for manipulation – as it is largely controlled bit the BIS (Bank for International Settlement, in Basle, Switzerland, also called the central bank of all central banks, and yes, the same bank that helped the FED finance Hitler’s war against the Soviet Union – so you see where this bank is coming from).

It is entirely privately owned and largely controlled by the Rothschild clan. And as an associated side note – few people talk about it, there is more than 100 times more paper gold in circulation than you could ever cash in, if you needed it. It is another one of those bank-invented bubbles that will explode and serve to enrich them when the time is ripe.

Bitcoins, the most prominent of some 3,000 to 4,000 cryptocurrencies flooding the world, is totally unreliable. A year after it was created in 2008 allegedly by an unknown person or group of people using the name Satoshi Nakamoto, bitcoin’s value in 2009 was US$ 0.08,

It gradually rose and eventually jumped in December 2017 briefly above US$ 20,000, but dropped within a year to about US$ 3,500. Today bitcoin is hovering around US$ 9,500 (August / September 2019). Bitcoin – along with other cryptocurrencies – is highly speculative, lends itself to Mafia-type money-laundering and other fraudulent transactions. It is about equivalent to fiat money and certainly inept to be the backing for a monetary system.

And let’s not forget, the latest Facebook initiative – a cryptocurrency, the Libra, to be launched in 2020 out of Geneva, Switzerland – is expected to dominate within a few years 70% to 80% of the international money market. You see, the same clan that has been manipulating and cheating you with the dollar, is now ‘banking’ on you falling for the Facebook currency – as it will be so easy to use your smart phone for any kind of monetary transaction, thus, avoiding traditional predatory banking. Looks like a good thing at the outside – right? – Nope! Its entirely privately owned and run by an unscrupulous mafia that is being set up to continue milking the masses for the benefits of an ever-smaller elite.

There is however a role for blockchain cryptocurrencies, to circumvent private banking, those that are government controlled and regulated. China and Russia are about to launch their government-controlled cryptocurrencies and others – Iran, Venezuela, India – are following in the same steps.

But they all ban privately run cryptocurrencies in their countries – and rightly so. A combination of government-regulated blockchain cryptos and public banking, where no private profits are in the fore, but rather the well being of the citizen and the country’s economy, may be a viable solution into a new monetary scheme, protected from the kleptocracy of western banking.

***

Desperation about the dollar losing its world hegemony is growing – and growing fast. To salvage the western fiat monetary system, Madame Lagarde and others are also talking about some kind of Special Drawing Rights (SDR) to replace the dollar as a reserve currency, since there is no escaping – the dollar as reserve currency is doomed.

The current IMF SDR basket consists of five currencies, the US-dollar (weighing 41.73%), the British Pound (8.02%) the Euro (30.93%), the Japanese Yen (8.33%) and since 2017 the Chinese Yuan, the currency of the world’s largest economy compared by Purchasing Power GDP (10.92%).

At this point thinking of any reshuffling of the SDR basket’s contents is purely speculative. However, it can easily be assumed that the dollar would remain in a very prominent position within the basket, as it should remain the leading hegemon of world economy. Let’s not forget, The US Treasury controls the IMF with an absolute veto, in other words – 100%.

It can also be assumed that the Chinese Yuan would either be kicked out altogether or would be given a minor weight in the basket, so to diminish its role. If this was to become the chosen option by the US Treasury, it could and probably might prompt China to withdraw the Yuan from the SDR basket, as the Yuan does no longer need SDR recognition in the world to be considered a primary reserve currency.

Unless this is stealthily done – outside of public sight and in disguise of countries still holding major US-dollar reserves, the world would unlikely accept such an alternative, especially since it is widely known among treasurers of countries around the globe that the Chinese Yuan is rapidly raising to become the key world reserve currency.

As reported by William Engdahl’s analytical essay “Is the Fed Preparing to Topple the US Dollar?” the outgoing Governor of the Bank of England, Mark Carney, delivered at the recent annual meeting of central bankers in Jackson Hole, Wyoming, a set of ideas that went into a similar direction, towards a shift away from the dominant role of the US dollar as a reserve currency. Similar to Mme.

Lagarde’s earlier remarks about an SDR-type reserve currency, he made it understood that though, the Chinese Yuan, the currency of the key trading nation, may have a role in the basket, it would – for now – not be an important one. He also was clear about the current disturbing and destabilizing imbalance – where a faltering dollar still pretends to hold the hegemonic scepter over the world economy.

Keeping the dollar still in a leading role, while the US economy is declining, was no longer a viable option for an increasingly globalized world economy. Carney was hinting at a multipolar monetary and reserve system for a multipolar globalized world.

Similar remarks came from former New York Federal Reserve Bank chief, Bill Dudley. However, Dudley, hinted that for the United States to give up her dollar dominance, the backbone for her world hegemony, may not come voluntarily. Might that lead to a major, maybe armed world conflict?

Much of this is speculation from the western perspective. It is however clear, that there is a tremendous and mounting uneasiness about the western, dollar-based fiat monetary system, backed by nothing, not even by the western economy.

You compare this with the Chinese and the Russian Ruble, both backed by gold and – more importantly – by their own economy. It becomes increasingly clear that much of the speculation and efforts by influential central banking figures to save the western monetary Ponzi scheme, maybe just propaganda to calm the minds of western financiers – holding them back from jumping ship.

Peter Koenig is an economist and geopolitical analyst. After working for over 30 years with the World Bank he penned Implosion, an economic thriller, based on his first-hand experience. Exclusively for the online magazine “New Eastern Outlook.”

www.veteranstoday.com/2019/09/17/neo-will-the-imf-fed-negative-interest-and-digital-money-kill-the-western-economy/

1 COMMENT

Gall September 17, 2019 at 3:50 pm

Time to launch a tactical nuke at the Fed and return to Article I Section 8.

|

|

|

|

Post by 3bid on Sept 20, 2019 3:08:55 GMT -5

Desperate Central Bankers Grab for More PowerPosted on September 18, 2019 by Ellen Brown Conceding that their grip on the economy is slipping, central bankers are proposing a radical economic reset that would shift yet more power from government to themselves. Central bankers are acknowledging that they are out of ammunition. Mark Carney, the soon-to-be-retiring head of the Bank of England, said in a speech at the annual meeting of central bankers in August in Jackson Hole, Wyoming, “In the longer-term, we need to change the game.” The same point was made by Philipp Hildebrand, former head of the Swiss National Bank, in an August 2019 interview with Bloomberg. “Really there is little if any ammunition left,” he said. “More of the same in terms of monetary policy is unlikely to be an appropriate response if we get into a recession or sharp downturn.” “More of the same” meant further lowering interest rates, the central bankers’ stock tool for maintaining their targeted inflation rate in a downturn. Bargain-basement interest rates are supposed to stimulate the economy by encouraging borrowers to borrow (since rates are so low) and savers to spend (since they aren’t making any interest on their deposits and may have to pay to store them). But over $15 trillion in bonds are now trading globally at negative interest rates, yet this radical maneuver has not been shown to measurably improve economic performance. In fact new research shows that negative interest rates from central banks, rather than increasing spending, stopping deflation, and stimulating the economy as they were expected to do, may be having the opposite effects. They are being blamed for squeezing banks, punishing savers, keeping dying companies on life support, and fueling a potentially unsustainable surge in asset prices. So what is a central banker to do? Hildebrand’s proposed solution was presented in a paper he wrote with three of his colleagues at BlackRock, the world’s largest asset manager, where he is now vice chairman. Released in August to coincide with the annual Jackson Hole meeting of central bankers, the paper was co-authored by Stanley Fischer, former governor of the Bank of Israel and former vice chairman of the U.S. Federal Reserve; Jean Boivin, former deputy governor of the Bank of Canada; and BlackRock economist Elga Bartsch. Their proposal calls for “more explicit coordination between central banks and governments when economies are in a recession so that monetary and fiscal policy can better work in synergy.” The goal, according to Hildebrand, is to go “direct with money to consumers and companies in order to enliven consumption,” putting spending money directly into consumers’ pockets. It sounds a lot like “helicopter money,” but he was not actually talking about raining money down on the people. The central bank would maintain a “Standing Emergency Fiscal Facility” that would be activated when interest rate manipulation was no longer working and deflation had set in. The central bank would determine the size of the Facility based on its estimates of what was needed to get the price level back on target. It sounds good until you get to who would disburse the funds: “Independent experts would decide how best to deploy the funds to both maximize impact and meet strategic investment objectives set by the government.” “Independent experts” is another term for “technocrats” – bureaucrats chosen for their technical skill rather than by popular vote. They might be using sophisticated data, algorithms and economic formulae to determine “how best to deploy the funds,” but the question is, “best for whom?” It was central bank technocrats who plunged the economies of Greece and Italy into austerity after 2011, and unelected technocrats who put Detroit into bankruptcy in 2013. In short, Hildebrand and co-authors are not talking about central banks giving up their ivory tower independence to work with legislators in coordinating fiscal and monetary policy. Rather, central bankers would be acquiring even more power, by giving themselves a new pot of free money that they could deploy as they saw fit in the service of “government objectives.” Carney’s New Game The tendency to overreach was also evident in the Jackson Hole speech of BOE head Mark Carney, in which he said “we need to change the game.” The game changer he proposed was to break the power of the US dollar as global reserve currency. This would be done through the issuance of an international digital currency backed by multiple national currencies, on the model of Facebook’s “Libra.” Multiple reserve currencies are not a bad idea, but if we’re following the Libra model, we’re talking about a new, single reserve currency that is merely “backed” by a basket of other currencies. The question then is who would issue this global currency, and who would set the rules for obtaining the reserves. Carney suggested that the new currency might be “best provided by the public sector, perhaps through a network of central bank digital currencies.” This raises further questions. Are central banks really “public”? And who would be the issuer – the banker-controlled Bank for International Settlements, the bank of central banks in Switzerland? Or perhaps the International Monetary Fund, which Carney is in line to head? The IMF already issues Special Drawing Rights to supplement global currency reserves, but they are merely “units of account” which must be exchanged for national currencies. Allowing the IMF to issue the global reserve currency outright would give unelected technocrats unprecedented power over nations and their money. The effect would be similar to the surrender by EU governments of control over their own currencies, making their central banks dependent on the European Central Bank for liquidity, with its disastrous consequences. Time to End the “Independent” Fed? A media event that provoked even more outrage against central bankers last month, however, was an August 27th op-ed in Bloomberg by William Dudley, former president of the New York Fed and a former partner at Goldman Sachs. Titled “The Fed Shouldn’t Enable Donald Trump,” it concluded: There’s even an argument that the [presidential] election itself falls within the Fed’s purview. After all, Trump’s reelection arguably presents a threat to the U.S. and global economy, to the Fed’s independence and its ability to achieve its employment and inflation objectives. If the goal of monetary policy is to achieve the best long-term economic outcome, then Fed officials should consider how their decisions will affect the political outcome in 2020. The Fed is so independent that, according to former Fed chair Alan Greenspan, it is answerable to no one. A chief argument for retaining the Fed’s independence is that it needs to remain a neutral arbiter, beyond politics and political influence; and Dudley’s op-ed clearly breached that rule. Critics called it an attempt to overthrow a sitting president, a treasonous would-be coup that justified ending the Fed altogether. Perhaps, but central banks actually serve some useful functions. Better would be to nationalize the Fed, turning it into a true public utility, mandated to serve the interests of the economy and the voting public. Having the central bank and the federal government work together to coordinate fiscal and monetary policy is actually a good idea, so long as the process is transparent and public representatives have control over where the money is deployed. It’s our money, and we should be able to decide where it goes. ______________________ This article was first posted on Truthdig.org. Ellen Brown chairs the Public Banking Institute and has written thirteen books, including her latest, Banking on the People: Democratizing Money in the Digital Age. She also co-hosts a radio program on PRN.FM called “It’s Our Money.” Her 300+ blog articles are posted at EllenBrown.com. ellenbrown.com/2019/09/18/desperate-central-bankers-grab-for-more-power/

|

|

|

|

Post by 3bid on Sept 23, 2019 23:30:42 GMT -5

‘Commit all the fraud you need as long as you support the US dollar’ – Max Keiser on JP Morgan scandal Published time: 22 Sep, 2019

The US authorities were aware that three JP Morgan traders were manipulating precious metals markets from the start and intentionally “looked the other way,” Max Keiser believes.

“Eric Holder, who was attorney general under [former US President Barack] Obama when this first came to light, said that market manipulation and fraud were important for the American economy and that he, as the attorney general, could not prosecute,” the host of RT’s Keiser Report says, calling the JP Morgan fraudsters and the likes “too big to jail.”

And that too-big-to-jail was part of the legal landscape for America, and bankers were getting a green light to commit massive fraud.

The fact that precious metals traders at JP Morgan made millions through fraudulent trades, operating a criminal conspiracy to manipulate prices called ‘spoofing’, has been an open secret for years, with Max himself describing the scheme back in 2011.www.rt.com/business/469340-jp-morgan-spoofing-keiser/

|

|

|

|

Post by 3bid on Nov 3, 2019 12:02:25 GMT -5

Gold, Credit And The Coming Financial Collapse

By Hubert Moolman

25 October 2019

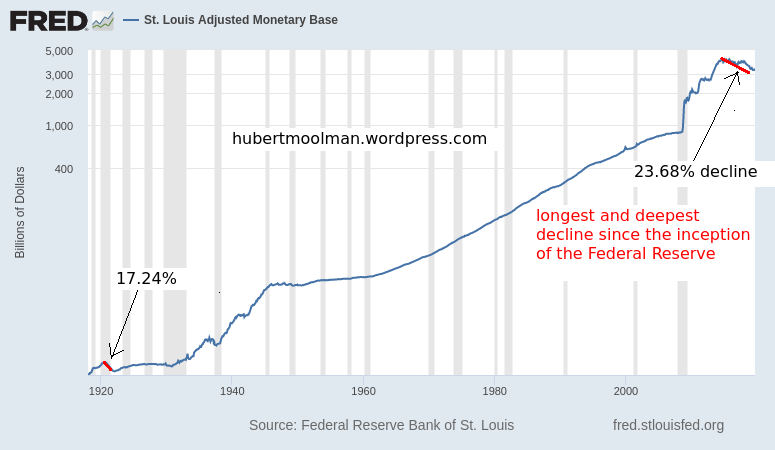

Since 2016, the US Monetary Base has declined by about 23.68%. This is the deepest and longest decline since the Federal Reserve was formed. This should not be ignored.

The last time there was a decline close to this magnitude,there was a sharp deflationary recession. That was the one that occurred from 1920 to 1921.

Below, is a long-term chart of the Monetary base that goes back to 1918: During the 1920-1921 recession the decline in the monetary base eventually made it into the broader money supply and this caused a significant drop in price levels (between 13% and 18%) during the recession, with wholesale prices dropping as much as 36%. During the 1920-1921 recession the decline in the monetary base eventually made it into the broader money supply and this caused a significant drop in price levels (between 13% and 18%) during the recession, with wholesale prices dropping as much as 36%.

The current decline in the monetary base has not evolved into a decline of the money supply yet, but it will likely soon do so. Especially if the economy goes into a recession and the stock market collapses.

The monetary base is the foundation part of the money supply, and represents the most liquid part of it. It basically acts like gold in a 100% funded gold standard: it represents the final settlement of a transaction.

If the monetary base is declining then less means to service debt is available and could trigger mass defaults. Cash becomes scarce and suddenly you have a situation where the Fed has to intervene in the repo market like it has been over the last couple of weeks, just to keep the system going.

This problem is not just going to go away without a major crisis and some severe consequences. By my estimation the banking system is broken and is unable to continue creating new credit in its current form, just like a bank is unable to increase its gold holdings under a gold standard when there is distrust of the banking system or that particular bank.

Believe it or not, the reserve banks do not control all the elements in the system: they are not all powerful and unstoppable. The appetite or ability to take on new credit is just not there anymore.

In my opinion, their intervention is not about making the crisis go away (because it won’t), but to protect their interest during the crisis.

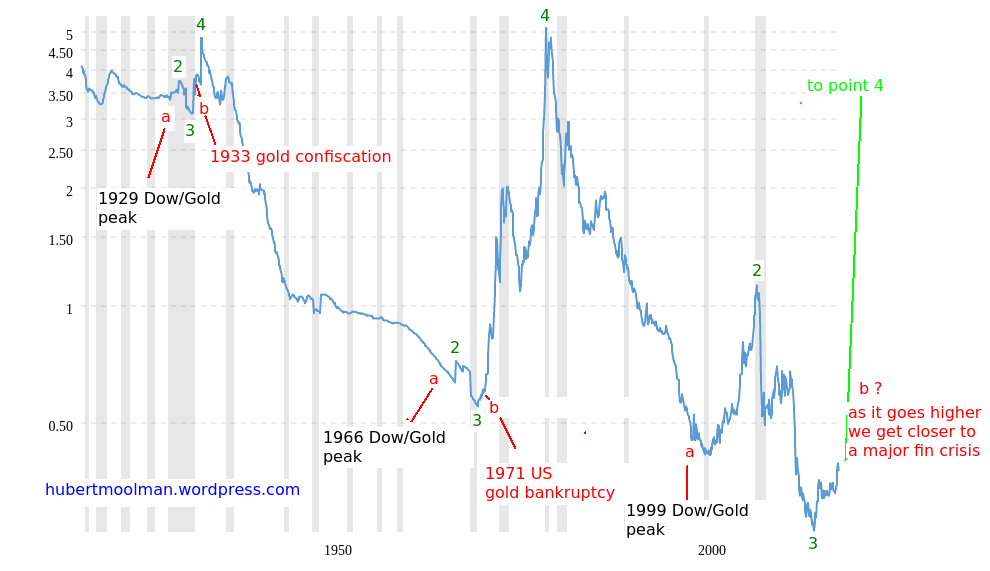

This is likely the beginnings of the expected monetary event I have pointed out before: The chart shows the ratio of the gold price to the St. Louis Adjusted Monetary Base back to 1918. That is the gold price in US dollars divided by the St. Louis Adjusted Monetary Base in billions of US dollars.(from macrotrends.com) The chart shows the ratio of the gold price to the St. Louis Adjusted Monetary Base back to 1918. That is the gold price in US dollars divided by the St. Louis Adjusted Monetary Base in billions of US dollars.(from macrotrends.com)

More details about the chart and original commentary here.

The bottom at point 3 is now virtually confirmed and we could soon have an event similar to the 1933 gold confiscation (bankruptcy) and the 1971 announcement where the US ended the dollar convertibility to gold (at a fixed rate).

Although both of the historic events were significant, they did not occur during a stock market crash or during a recession. There is a huge potential that the coming event could happen during a major stock market crash and recession.

Therefore, the coming monetary event could be the cause (or at the center) of the coming crisis, whereas with the previous two they were as a result of an ongoing crisis, and came towards the end to “correct” the situation.

Note that a sharp move from point 3 to point 4 on the chart is akin to a bank run on gold holding banks in a gold standard. With the decline in the monetary base and a rising gold price this is exactly what is happening.hubertmoolman.wordpress.com/2019/10/25/gold-credit-and-the-coming-financial-collapse/

|

|

|

|

Post by 3bid on Nov 13, 2019 9:04:51 GMT -5

The World Has Gone Mad and the System Is Broken

Ray Dalio

I say these things because:

Money is free for those who are creditworthy because the investors who are giving it to them are willing to get back less than they give. More specifically investors lending to those who are creditworthy will accept very low or negative interest rates and won’t require having their principal paid back for the foreseeable future. They are doing this because they have an enormous amount of money to invest that has been, and continues to be, pushed on them by central banks that are buying financial assets in their futile attempts to push economic activity and inflation up. The reason that this money that is being pushed on investors isn’t pushing growth and inflation much higher is that the investors who are getting it want to invest it rather than spend it. This dynamic is creating a “pushing on a string” dynamic that has happened many times before in history (though not in our lifetimes) and was thoroughly explained in my book Principles for Navigating Big Debt Crises. As a result of this dynamic, the prices of financial assets have gone way up and the future expected returns have gone way down while economic growth and inflation remain sluggish. Those big price rises and the resulting low expected returns are not just true for bonds; they are equally true for equities, private equity, and venture capital, though these assets’ low expected returns are not as apparent as they are for bond investments because these equity-like investments don’t have stated returns the way bonds do. As a result, their expected returns are left to investors’ imaginations. Because investors have so much money to invest and because of past success stories of stocks of revolutionary technology companies doing so well, more companies than at any time since the dot-com bubble don’t have to make profits or even have clear paths to making profits to sell their stock because they can instead sell their dreams to those investors who are flush with money and borrowing power. There is now so much money wanting to buy these dreams that in some cases venture capital investors are pushing money onto startups that don’t want more money because they already have more than enough; but the investors are threatening to harm these companies by providing enormous support to their startup competitors if they don’t take the money. This pushing of money onto investors is understandable because these investment managers, especially venture capital and private equity investment managers, now have large piles of committed and uninvested cash that they need to invest in order to meet their promises to their clients and collect their fees.

At the same time, large government deficits exist and will almost certainly increase substantially, which will require huge amounts of more debt to be sold by governments—amounts that cannot naturally be absorbed without driving up interest rates at a time when an interest rate rise would be devastating for markets and economies because the world is so leveraged long. Where will the money come from to buy these bonds and fund these deficits? It will almost certainly come from central banks, which will buy the debt that is produced with freshly printed money. This whole dynamic in which sound finance is being thrown out the window will continue and probably accelerate, especially in the reserve currency countries and their currencies—i.e., in the US, Europe, and Japan, and in the dollar, euro, and yen.

At the same time, pension and healthcare liability payments will increasingly be coming due while many of those who are obligated to pay them don’t have enough money to meet their obligations. Right now many pension funds that have investments that are intended to meet their pension obligations use assumed returns that are agreed to with their regulators. They are typically much higher (around 7%) than the market returns that are built into the pricing and that are likely to be produced. As a result, many of those who have the obligations to deliver the money to pay these pensions are unlikely to have enough money to meet their obligations. Those who are recipients of these benefits and expecting these commitments to be adhered to are typically teachers and other government employees who are also being squeezed by budget cuts. They are unlikely to quietly accept having their benefits cut. While pension obligations at least have some funding, most healthcare obligations are funded on a pay-as-you-go basis, and because of the shifting demographics in which fewer earners are having to support a larger population of baby boomers needing healthcare, there isn’t enough money to fund these obligations either. Since there isn’t enough money to fund these pension and healthcare obligations, there will likely be an ugly battle to determine how much of the gap will be bridged by 1) cutting benefits, 2) raising taxes, and 3) printing money (which would have to be done at the federal level and pass to those at the state level who need it). This will exacerbate the wealth gap battle. While none of these three paths are good, printing money is the easiest path because it is the most hidden way of creating a wealth transfer and it tends to make asset prices rise. After all, debt and other financial obligations that are denominated in the amount of money owed only require the debtors to deliver money; because there are no limitations made on the amounts of money that can be printed or the value of that money, it is the easiest path. The big risk of this path is that it threatens the viability of the three major world reserve currencies as viable storeholds of wealth. At the same time, if policy makers can’t monetize these obligations, then the rich/poor battle over how much expenses should be cut and how much taxes should be raised will be much worse. As a result rich capitalists will increasingly move to places in which the wealth gaps and conflicts are less severe and government officials in those losing these big tax payers will increasingly try to find ways to trap them.

At the same time as money is essentially free for those who have money and creditworthiness, it is essentially unavailable to those who don’t have money and creditworthiness, which contributes to the rising wealth, opportunity, and political gaps. Also contributing to these gaps are the technological advances that investors and the entrepreneurs that I previously mentioned are excited by in the ways I described, and that also replace workers with machines. Because the “trickle-down” process of having money at the top trickle down to workers and others by improving their earnings and creditworthiness is not working, the system of making capitalism work well for most people is broken.

This set of circumstances is unsustainable and certainly can no longer be pushed as it has been pushed since 2008. That is why I believe that the world is approaching a big paradigm shift.

www.linkedin.com/pulse/world-has-gone-mad-system-broken-ray-dalio/

|

|

|

|

Post by 3bid on Jan 26, 2020 13:33:12 GMT -5

How cash is becoming a thing of the past (Banking documentary)

Published on Nov 21, 2018 | DW Documentary

Cashless payments are on the rise. They are fast, easy and convenient. Worldwide, cashless transactions have become the norm.

But Germany’s central bank and government are still clinging on to cash. Can they stop the move towards a cashless society? Our documentary shows who is behind the worldwide anti-cash lobby. Banks want to get rid of coins and bills for cost reasons, and politicians think less cash will cut the rug out from under criminals and terrorists. Central bankers want to abolish cash because it would make it easier for them to enforce negative interest rates. And digital payment companies like Paypal or Visa simply want to profit from money transactions and collect as much financial data about consumers as they can. Their aim is to gain complete control over our buying behavior. For example, the "Better than Cash Alliance" in New York is supported by financial corporations such as Visa or Mastercard. They say the more people that are integrated into the international financial system, the more growth and jobs it will promote. But as our financial behavior becomes more and more transparent, states are also using payment data to find out more about us. The ordinary citizen’s view of cash as a store of value, independent of third party interests, is being increasingly ignored. But for them, cash is and will remain a symbol of freedom.

|

|

|

|

Post by 3bid on Apr 29, 2020 10:11:01 GMT -5

Matt Taibbi: Why this bailout is worse than 2008

Published on Apr 10, 2020

Author and reporter Matt Taibbi explains how corporate America will over-indulge on its piece of the $2 trillion dollar bailout package, thus creating another financial catastrophe.

|

|

|

|

Post by 3bid on Jun 17, 2020 12:28:52 GMT -5

US bankers stole $7 trillion during COVID-19 lockdown, destroyed small businesses

By Kevin Barrett - June 16, 2020

[...]

US bankers conducted the biggest heist in history

The mainstream media seems to be part of a propaganda operation that is trying to change the conversation right now from what really matters, which is that the most powerful banking cabal in the world — the people who essentially own and operate the government of the United States, the West and much of the world — just stole at least $7 trillion, primarily from poor people, in the COVID lockdown which destroyed small businesses all over the world, which is starving poor people all over the world, and which led to the printing of unlimited money for the world’s biggest and wealthiest bankers. It bailed them out of their debt crisis and gave them the right to give themselves and their friends as much money as they want by printing it out of thin air, and they are doing that even as we speak.

There was a corporate bailout at the level of trillions for the friends of Steven Mnuchin. He and his Zionist buddies have an unlimited credit line. They never have to pay it back. It’s basically just a bailout slush fund.

So this is the biggest robbery in the history of the world, and ordinary people are suffering horribly. They were locked down and they felt like they couldn’t breathe. Their economic lives have been destroyed and they felt like they couldn’t breathe. And so then suddenly, just at the moment when they should have risen up and revolt and stormed Wall Street, stormed Washington DC and overthrown these thieves who just conducted the biggest robbery in the history of the world, suddenly the conversation changes to race, and the ordinary working white people and black people are being turned against each other, talking about race, rather than this robbery, conducted under the premeditated pretext of a COVID pandemic which was almost certainly manufactured in a biological warfare lab, under the direction of the very bankers who have stolen six, seven or more trillion dollars based on this plandemic which they obviously plotted out in great detail ahead of time, as part of an effort for them to centralize their wealth and power to stop the rise of China by blowing up the globalized world with the economy that is the engine of China’s rise ,and to allow them to impose a top-down police state on the people of the West so they cancontinue to centralize and strengthen their control of the West and the world. That’s what COVID really was. And they’ve changed the conversation to race so we don’t notice it.

...........................................................................................

TimothyMadden June 17, 2020 at 1:25 am

Also don’t forget the systemic crippling of small business by deliberately mislabeled “Merchant Fees” on broadly-defined payment cards. Your “free loan” and “grace period” on a credit/charge-card transaction, for example, based on a 5% Merchant Fee and a 21-day “grace period” puts a 5% concealed interest charge in the card-issuer’s pocket at an effective interest rate of 144% per annum. All the card-issuers are required to – and do – treat them internally as interest / credit charges received from the card-users from whom they actually receive them. If the card-user doesn’t pay then the bank never receives the “Merchant Fee” and that reality of credit cannot be avoided by a label.

Technically the merchant is required to give a stipulated percentage “price discount” to a card-user (from 1% to 6%) but is also forbidden to tell them about it. the card-issuer then receives and books the concealed credit charge at the end of the grace period as a rake-off from the card-user’s payment.

These fees (concealed-credit-charges) are a percentage of the gross charge and are divvied-up among the card-issuer’s bank, the card-user’s bank, and the so-called clearinghouse. Then add the separate fixed direct monthly equipment fees to the merchant and the grand total in many cases can be up to 50% of the working capital (gross margin) of a small business.

With the surge in card-use from the coronavirus lockdown the global total will likely have passed the the USD-equivalent of $1 trillion per year ($1,000,000,000,000) or about $3 billion a day.

The article is correct in that a great deal of what is going on is targeted at small business.

oakwood June 17, 2020 at 12:28 am

Sometimes understatement carries more impact. Well said. The Chinese are playing the Anglo-Zionists as they have studied the power of the occupiers. China while not perfect and has corruption , makes sure the money they print mostly goes into vast infrastructure projects and employment and services. Wall Street has stashed the peoples trillions in offshore havens and in their bunkers and mansions which some are already fleeing to.[Patagonia] But they cannot drive their Veyrons down broken roads and collapsed bridges chased by millions of waking up starving zombies and where do they buy parts materials and lumber if the hardware stores are all looted and burned.. Also their body guards in time will start eyeing their wives and daughters and it will game over. Just like Rome and Venice history keeps repeating itself.

www.veteranstoday.com/2020/06/16/7-trillion/

|

|

|

|

Post by vulcanized crawler on Jun 17, 2020 13:17:09 GMT -5

not sure if 911 twin towers was a bigger bank robbery as the largest vault in the world got buried and everything went somewhere but, who knows where.

|

|

|

|

Post by Brigantine on Jun 19, 2020 15:00:36 GMT -5

yeah, like that gold didn't get emptied from those vaults on 9/10, right?

9/11 = largest gold robbery in history.

|

|